February 2026 Real Estate Market Update

February 15, 2026

Articles for Buyers

February 15, 2026

Articles for Buyers

This month we really want to focus on affordability, because it is improving. Mark Fleming, the Chief Economist at First American, said this: The forces that eroded affordability in the aftermath of the pandemic - strong price appreciation and surging mortgage rates - have stabilized. Moderating house price growth, easing mortgage rates, and steady income gains signal a realignment in the forces driving affordability trends.

Improving affordability is great news for real estate.

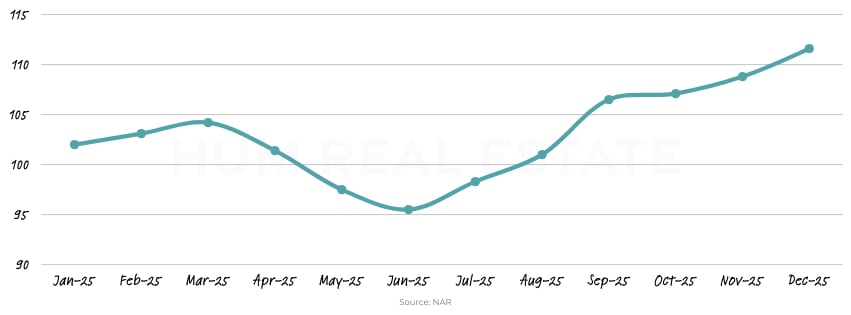

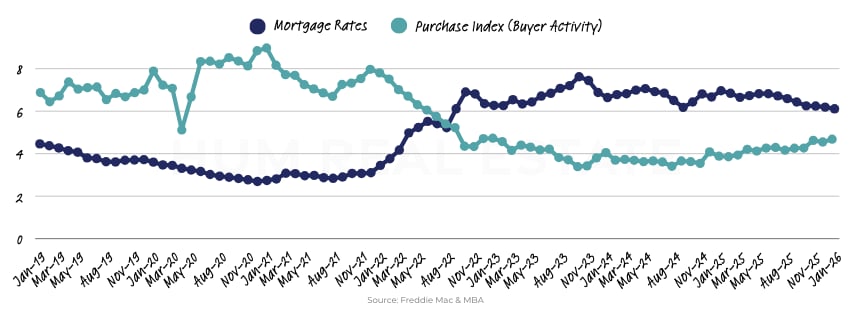

Affordability is signaled by 3 things: Mortgage rates, home prices, and wages. The National Association of Realtors® publishes an Affordability Index.

Affordability really improved in the second half of 2025 – starting in June, and really progressing from there. To be clear, this does not mean homes are magically affordable again, but we are seeing a trend moving in the right direction as mortgage rates come down, prices cool, and wages increase.

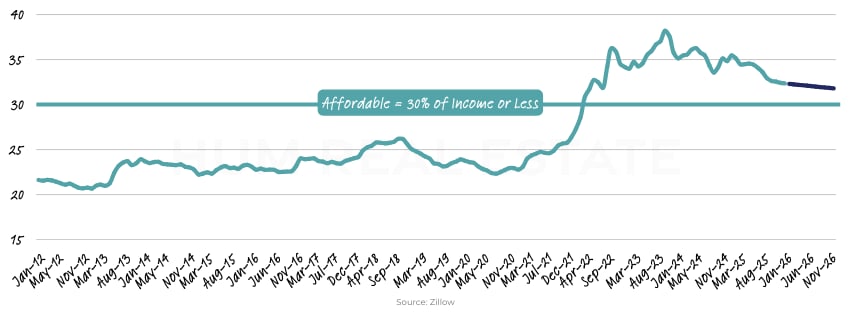

In fact, Zillow just said that: At the national level, a mortgage payment now takes 32.6% of median household income, already the best affordability seen nationwide since August 2022. That's on track to improve to 31.8% by the end of the year.

What happened after the pandemic is that affordability eroded as we saw higher prices and increasing mortgage rates. The peak of unaffordability occurred in October 2023, and since then we have been on a rocky road trying to get back to where people are spending 30% or less of their income on a home.

What’s even better news is that the current 32.6% of median household income it takes to be in a home now, and the 31.8% projection of what it will be by the end of the year, both include taxes, insurance, and maintenance. So, these are real numbers. They include the things that most people either think (1) make owning a home unaffordable, or (2) are not included in the statistics for affordability.

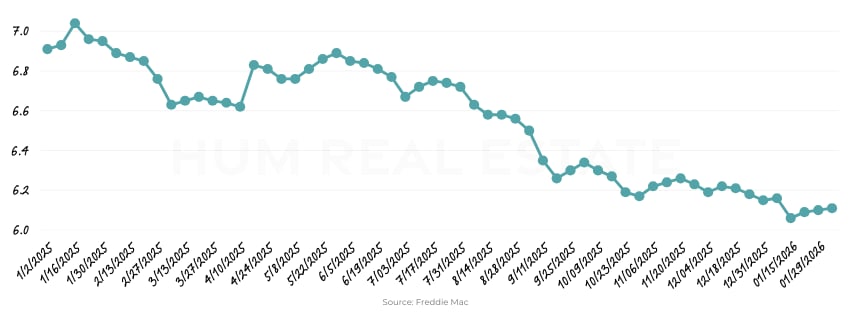

Mortgage rates not only came down significantly last year, but are near their lowest level in 3 years.

And they are not expected to fluctuate much in the near future.

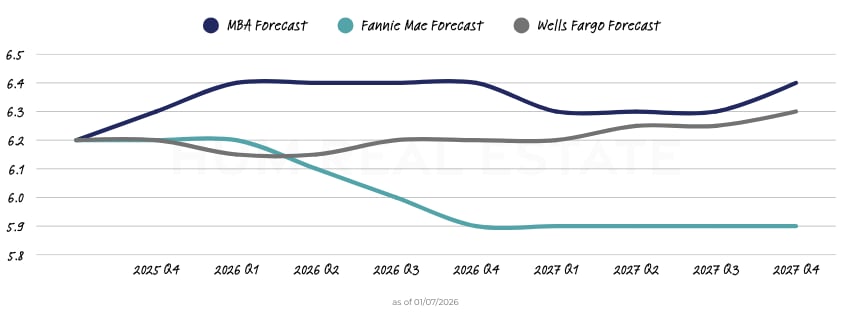

Let’s say that you wait for that Fannie Mae projected 5.9% at the end of 2026 or at the beginning of 2027… To put that into perspective, for the average priced home in Tallahassee ($344,020), you would save about $45 on your monthly payment. In addition, you would not be earning equity in your home in the time you wait. The real question becomes: Would you let $45 a month stop you from buying a home?

Just know that trying to time the market based on mortgage rates will not only be risky, but in that time home prices will increase. Home prices not only increase because they just do so over time, but, in the case of lower mortgage rates, because there are more buyers in the market – which mean more competition.

And more competition puts an upward pressure on prices. This is especially exaggerated in areas where housing inventory is tight, and there are not enough home on the market to support the demand.

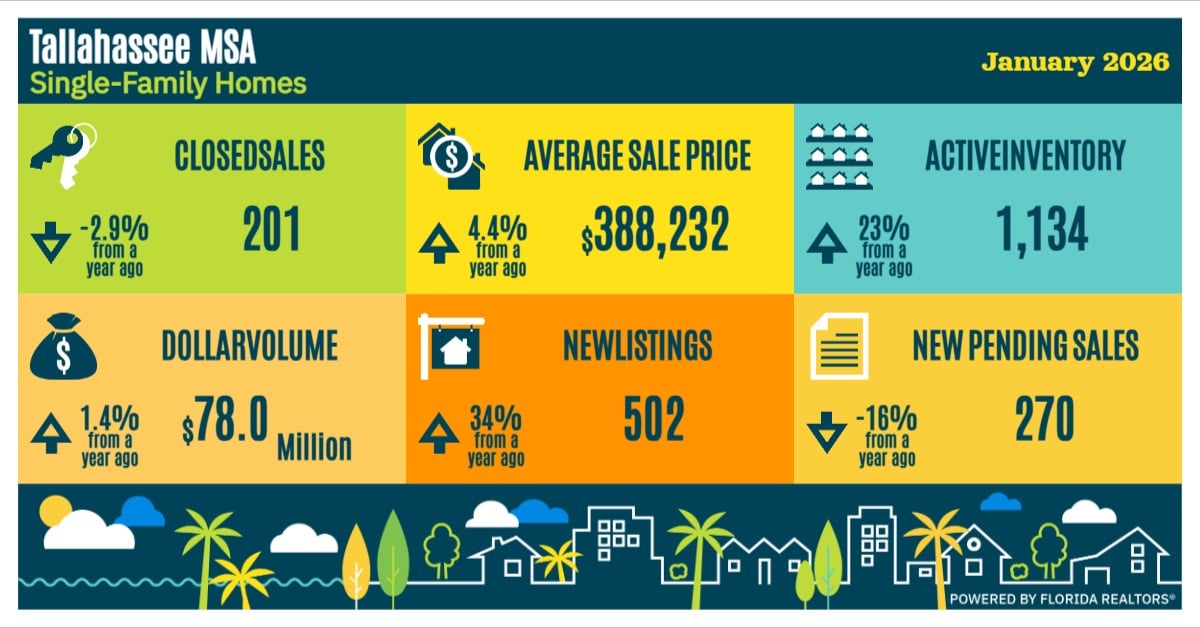

According to the latest figures from Florida Realtors®, in Tallahassee we sit at just 3.3 months of inventory on hand.

This means that if no more homes were listed for sale, it would take 3.3 months to sell all the inventory we have. It is said that a balanced market – in which sellers nor buyers have the upper hand, and there is enough inventory for the demand – should have between 4 and 6 months inventory on hand. This would be a healthy market. When areas see inventory below 4 to 6 months, that upward pressure on prices is in play.

Now, inventory does have a sort of cyclical trend, where we see higher figures in the peak season of summer. However, at the peak last year Tallahassee only saw 4.1 months inventory on hand. Locally, the last time we saw inventory at or above 4.1 months was in August of 2019. That was almost 7 years ago! To recover from inventory levels that low, and sustained for such a long period, it will take time to get back to a balanced market.

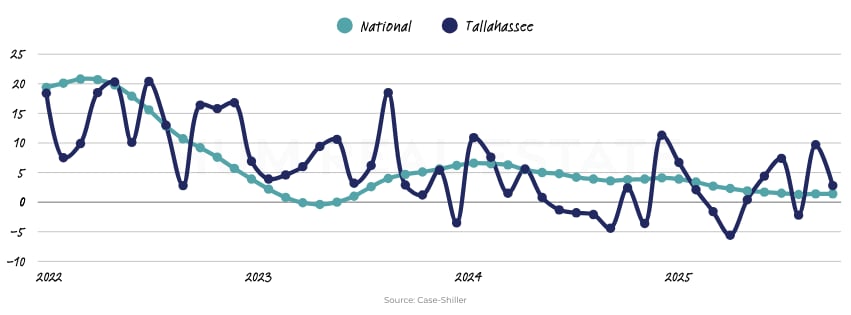

Mortgage rates were the first component of affordability, and we are seeing those come down. Home prices are the second component, and home price growth is also moderating.

Cooling home prices is more great news for affordability.

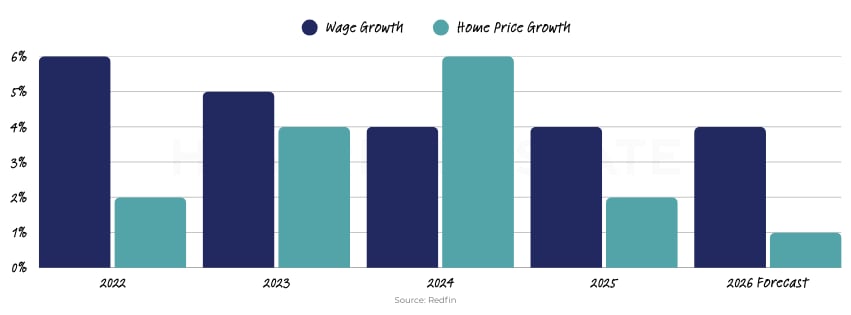

Finally, the third component of affordability is wages. Home price appreciation recently fell below the pace of income growth – which is good. That means wages are growing faster than home prices.

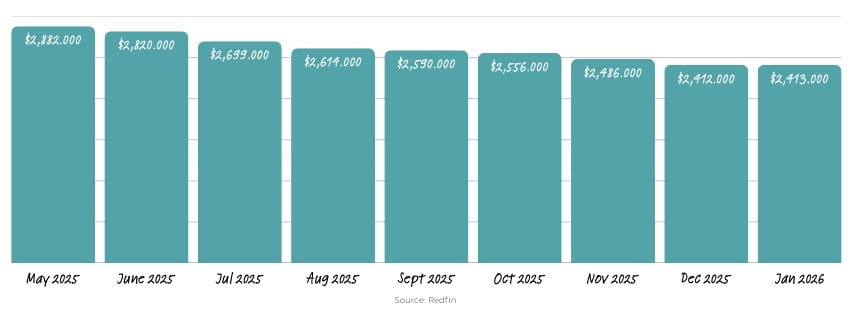

The average monthly mortgage payment is trending down.

This is primarily due to mortgage rates easing.

As far as what is to come for affordability, we quote Mark Fleming again to help determine what that might look like in 2026:

“Affordability remains challenging, but for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

Stay up to date on the latest real estate trends.

All Real Estate News

August 4, 2026

All Real Estate News

August 3, 2026

All Real Estate News

July 30, 2026

All Real Estate News

July 29, 2026

All Real Estate News

July 28, 2026

All Real Estate News

July 27, 2026

You’ve got questions and we can’t wait to answer them.