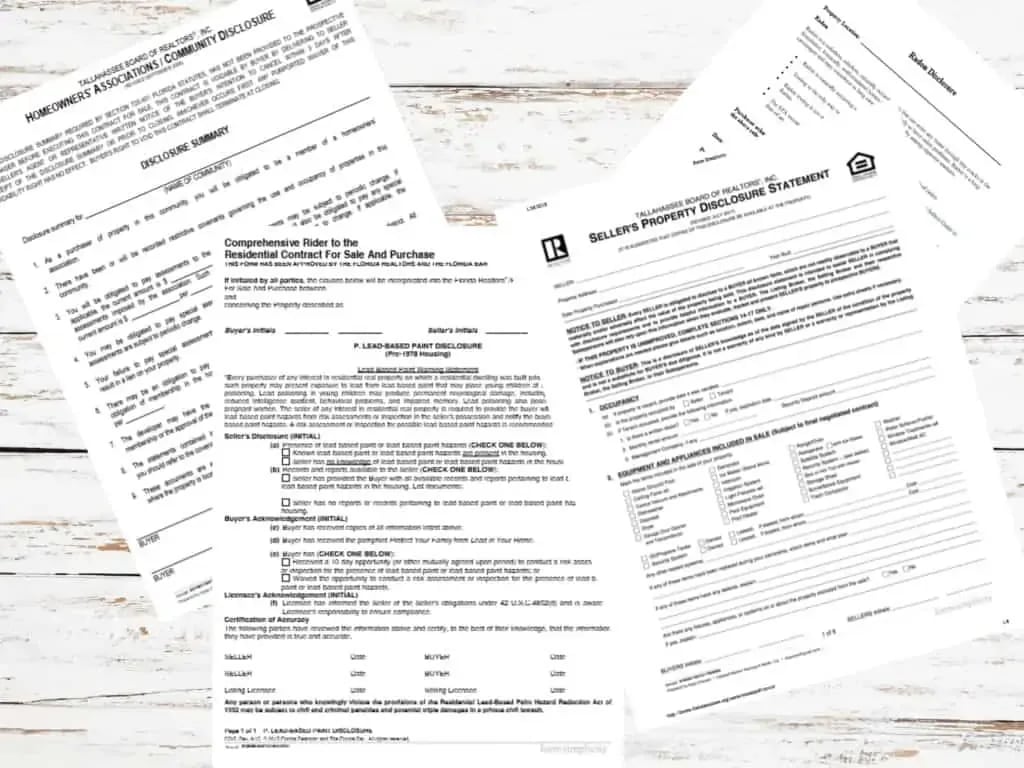

Before making an offer, your agent should create a detailed Comparative Market Analysis on the home to determine the best offer price. You will then meet to review the Sale and Purchase Agreement. This document includes information like the price offered, financing terms, the earnest money deposit, contingencies, and the closing date.

The earnest money deposit is most often 1% of the purchase price, and can be delivered on the contract date, or up to a few days after. It is deposited into an escrow account until the closing date, at which point the money is typically applied to the your costs at closing.

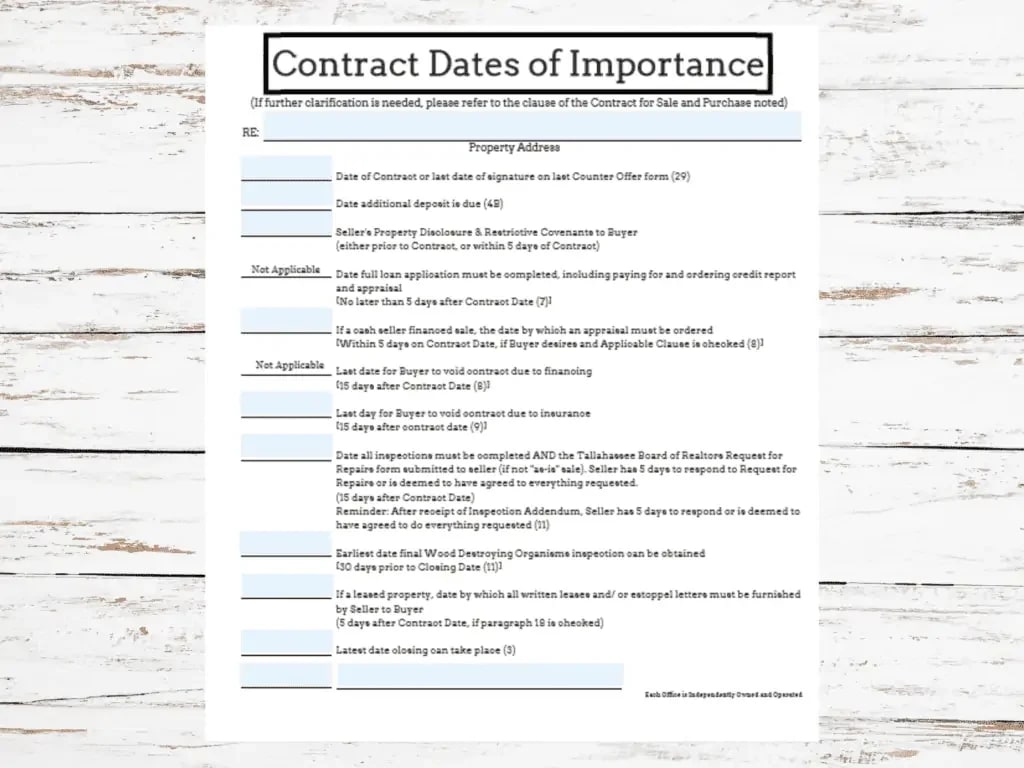

Contingencies are based on the satisfaction of things like the appraisal, inspections, insurability, and financing. Your agent should take the time to review each clause in detail, because failure to abide by the terms of the agreement could place your earnest money deposit as risk. Your agent and their team should keep you reminded of the important contractual obligations and their respective due dates along the way.

Upon receipt of your offer, the seller may accept, counter, or reject the presented contract. This isn't always about the highest offer price, but may be about specific terms - it is all dependent on the motivation of the seller.

The best offer will have the most preferable price, terms, and closing timeline, but there are ways to give yourself an advantage. Things that tend to be prudent in strengthening your offer are:

- Working with local lenders

- Increasing your earnest money deposit

- Shortening contingency periods

- Being flexible with the closing date

- Adding an escalation clause

Dealing with a rejected offer can be frustrating, but it is a great way to learn if the strategy needs to be re-examined.

It is important to note that negotiations may come into play again after the appraisal, inspections, and financing processes.