November 2025 Real Estate Market Update

November 29, 2025

All Real Estate News

November 29, 2025

All Real Estate News

This year, the unsung hero of the real estate market has been the lower trend of mortgage rates.

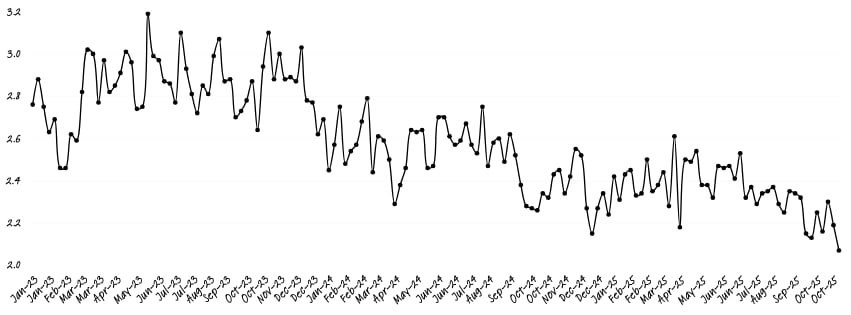

What’s even better news is that the spread (or difference) between the 10-year treasury yield and 30-year mortgage rate has been closing. Historically, and over the past 50 years, the spread between these two figures has been 1.7% (or 170 basis points). This means, if the 10-year treasury yield is 8%, the 30-year mortgage rate is about 6.3%. This difference represents uncertainty in the market, so, as it grows, that indicates maybe some turmoil or a lack of consumer confidence. Since the beginning of 2023, the spread between the 10-year treasury yield and 30-year mortgage rate has been about 3% (or 300 basis points) – not a great sign. However, the spread is now just 2% - indicating more confidence in the market or an acceptance of the “new normal.”

That is great news, because the lower this spread is, the lower the mortgage rate is.

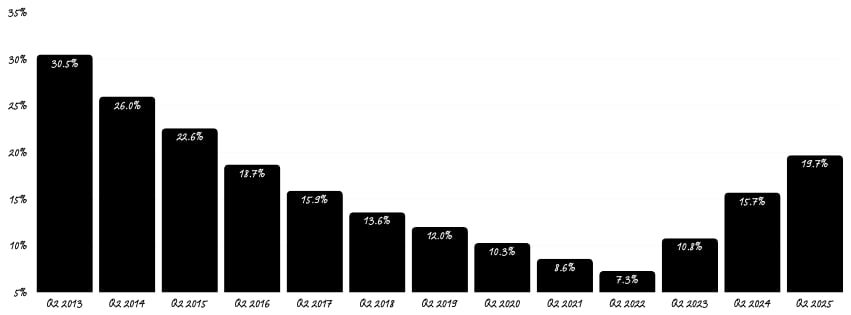

Every winner in the November elections this month mentioned housing affordability – showing this is a major concern across the board right now. A recent Redfin study that said only 28 out of a thousand US homes have changed hands in 2025. This is the lowest turnover rate in 30 years.

Now, it is important not to confuse tenure with turnover. Tenure is how long people stay in their homes. Turnover is how many homes are selling, or the velocity of home sales as compared to population growth. Right now, we are at about 4 million homes sold on the existing home sales report. This is a number we have seen over many years in the past, but it’s different because of the incredible population growth we have had.

The turnover rate is calculated by taking the number of homes sold averaged out per 1,000 households. Essentially, how many homes have sold per 1,000 homes.

As we await the numbers for October, we should see a bit more of a sales pace considering the recent drops in mortgage rates. Either way, this year will likely go down as one of the slowest years for home sales when adjusted for population growth – even though we’ll most likely sell more homes than we did last year.

Affordability challenges that have kept buyers on the sidelines, and sellers are unwilling to give up their low mortgage rates. 70% of homeowners have a rate below 5%. On top of that,

economic uncertainty has made buyers cautious.

None of this is to say the housing market is frozen. It’s all about perspective. With 4 million homes sold at an annualized rate, that means 11,123 houses sell each day in this country, and 463 sell per hour. That's no small feat.

In light of the saying that the headlines do more to terrify than they do to clarify, let’s take a look at the corner the housing market is turning. According to the VP and Deputy Chief Economist for First American, “After a prolonged slump, the existing-home market is showing signs of recovery.”

We're starting to see the market start to shift going into 2026. There are really three reasons for this. First, mortgage rates have been decreasing for most of this year, and they're lower than they've been in the last couple of years. Second, the lock-in effect is easing. More homeowners are selling and inventory is rising to a more historically normal level - that means there's more options. Finally, the combination of lower rates and more homes to choose from is leading more buyers into the market.

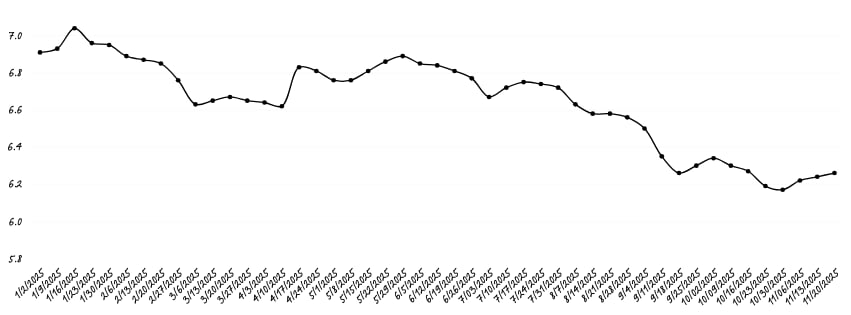

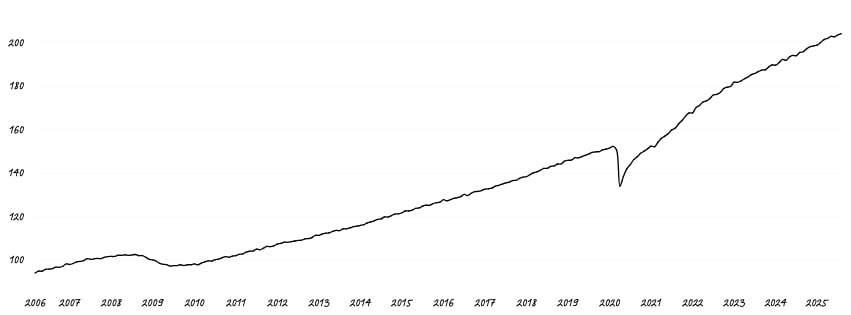

Mortgage rates are coming down. The Intercontinental Exchange said, “Home affordability hit its best level in more than 2.5 years in September, driven by easing rates and a pullback in prices.”

Based strictly on mortgage payments, affordability has improved. The median monthly mortgage payment peaked in May of the year, and has come down significantly.

Remember, there are 3 things that affect the monthly mortgage payment: First is the mortgage rate that's paid on the home - that's one of the biggest factors. And, where are rates at? They have come down. That's good for affordability.

The second thing is home prices – probably the biggest issue. There has been a dramatic rise in prices over the last few years. They're not rising at the pace they were coming out of COVID, but still a factor affecting affordability.

The third factor in affordability is wages. Wages are climbing at a faster pace than what the last decade or so has shown us. That's a good thing.

However, all that said, affordability is still a massive challenge, but we do see signs that we're heading in the right direction.

As of last week, the average 30-year mortgage rate was at 6.26%, and the median household income to make the monthly principal and interest payment was 30% - down from 32% earlier this summer. Although that is still too high, we're starting to see some signs that that's improving.

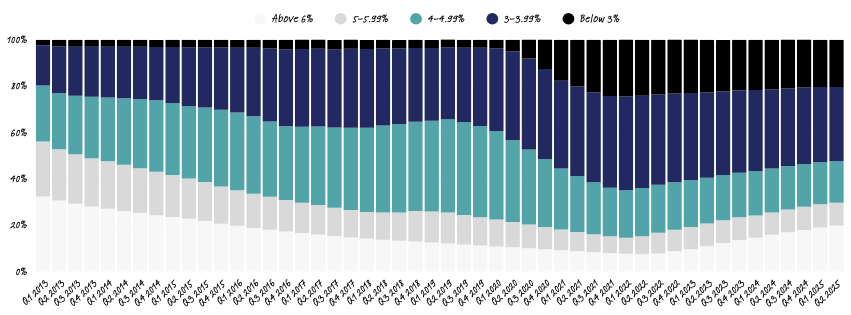

The other thing that is coming up in the news is that the rate lock effect in mortgages across is weakening. We can see this by looking at the share of outstanding residential mortgages and the rate they had at origination.

Essentially, loans with an original mortgage rate above 6% are rising. A recent Redfin study shows that more homeowners are deciding it's worth moving - even if that means giving up a lower mortgage rate. Life doesn't stand still. People get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefits of clinging onto a low mortgage rate.

The share of mortgages with a rate above 6% is climbing, for sure. Right now, it's close to 20%. This is part of the shift we are starting to see, and certainly a sign that things are changing in the real estate market.

As we already mentioned, inventory is continuing to grow.

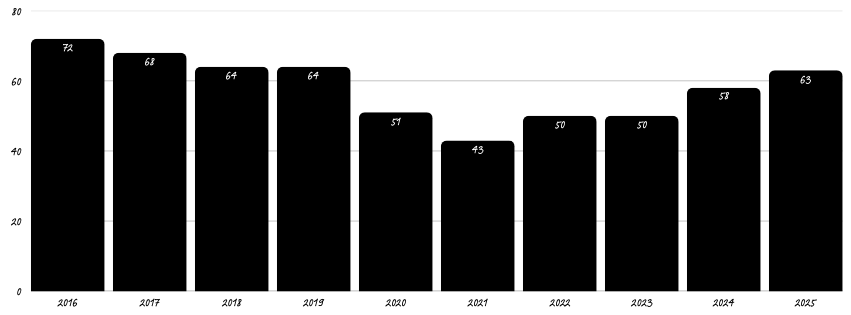

October marked the sixth month of active inventory (or homes for sale) above a million units. That’s great news, as the goal is to return to pre-pandemic inventory levels. In addition, purchase applications remained about 20% higher than a year ago. This all lends a hand to the fact that homes are now selling at a more normal pace of 63 days – the median number of days a home is on the market.

However, with this market shift, we are also seeing more price cuts.

As far as projections into next year, we are expected to see more homes sold.

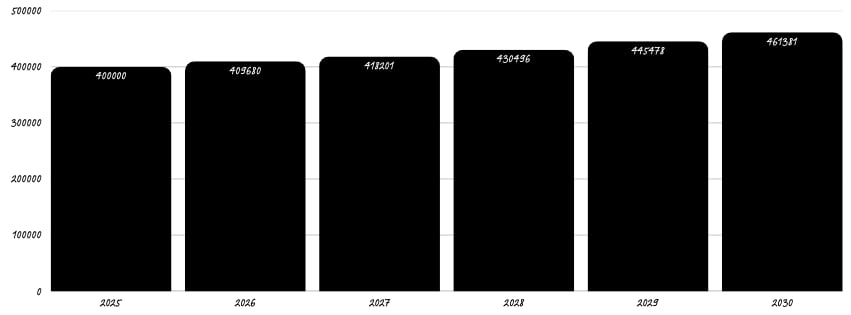

And homes are still expected to appreciate in value. Potential wealth of buying a $400,000 home today is about $61,381 over the next 5 years.

That is the equity a buyer could gain in just 5 years.

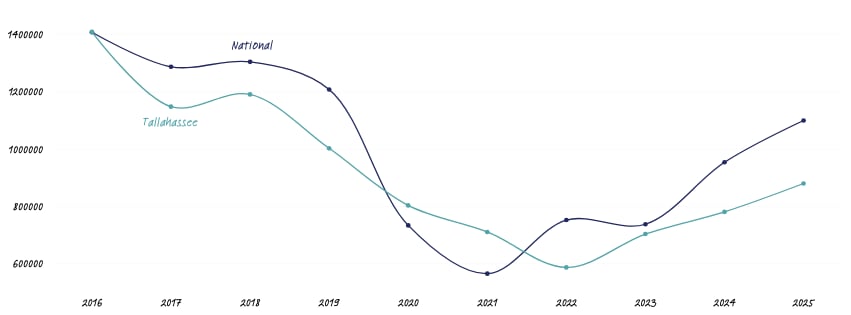

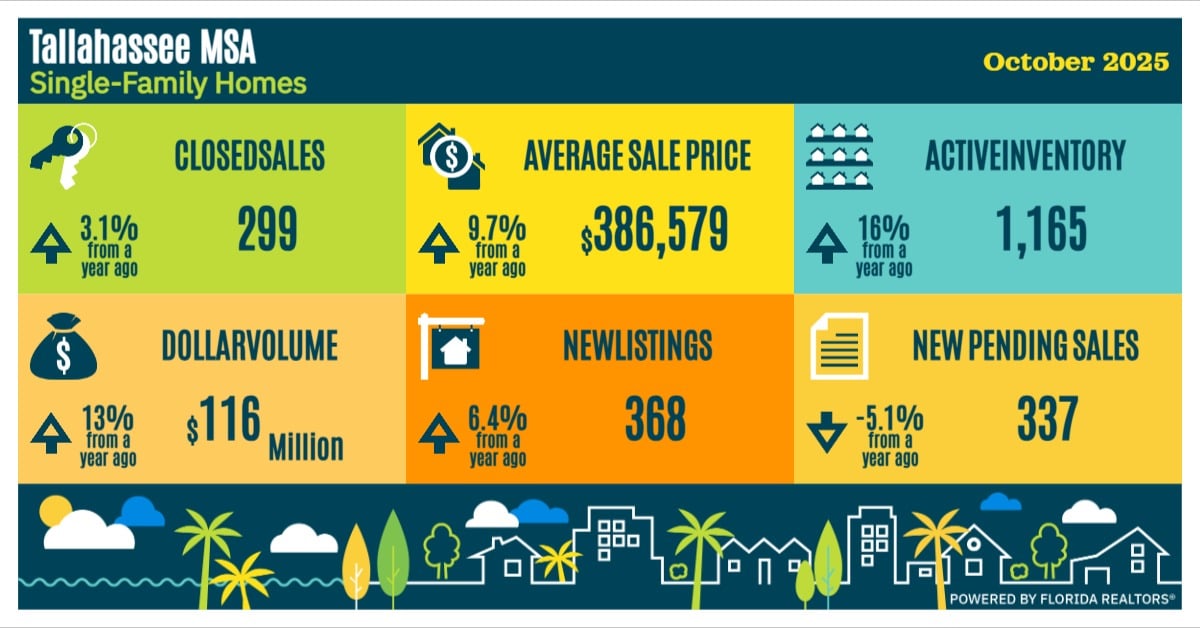

As always, we take a look back at how Tallahassee wrapped up last month:

Stay up to date on the latest real estate trends.

All Real Estate News

June 25, 2026

All Real Estate News

June 24, 2026

All Real Estate News

June 23, 2026

All Real Estate News

June 22, 2026

All Real Estate News

June 18, 2026

All Real Estate News

June 17, 2026

You’ve got questions and we can’t wait to answer them.