October 2022 Real Estate Market Update

October 17, 2022

Monthly Market Updates

October 17, 2022

Monthly Market Updates

There is much economic uncertainty, and a lot going on in the housing marketing right now. It is a very pivotal time for both buyers and sellers, so we are going to focus this month on some of the top real estate questions.

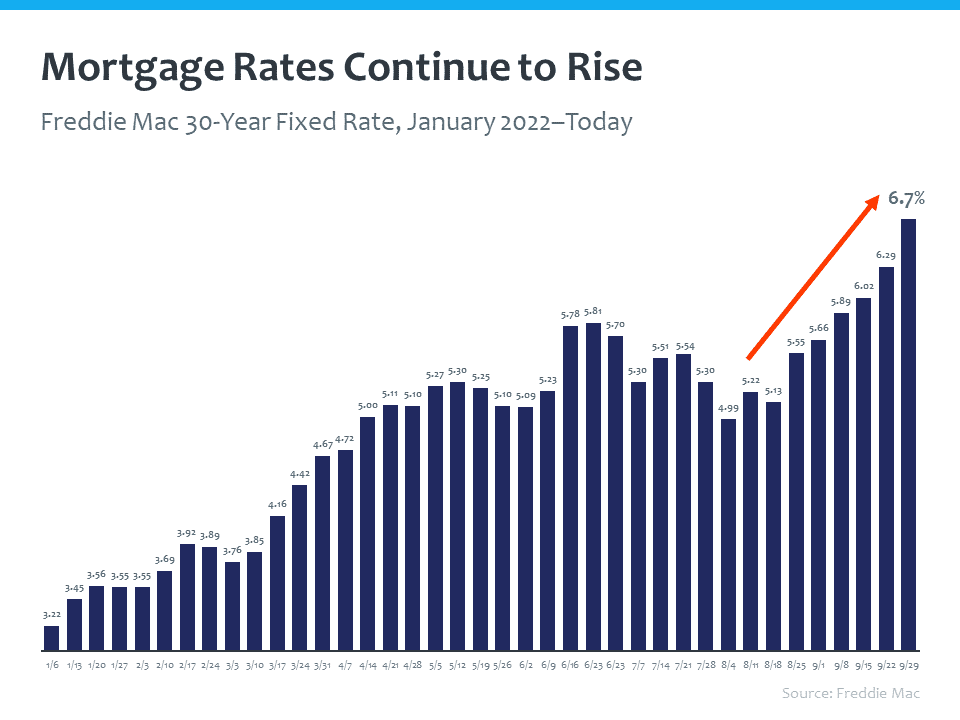

Let’s start with the rising interest rate environment we are in right now.

Mortgage rates have been rising since the beginning of the year, with a sharp incline over the past several weeks. There is a definite trend in an upward direction.

The Federal Reserve is trying to bring down inflation by slowing the economy, which is having an impact on mortgage rates. When inflation is high, mortgage rates tend to be high as well. Until inflation is down significantly, mortgage rates will rise, and demand will fall. Mortgage rates are likely increase over the next few months.

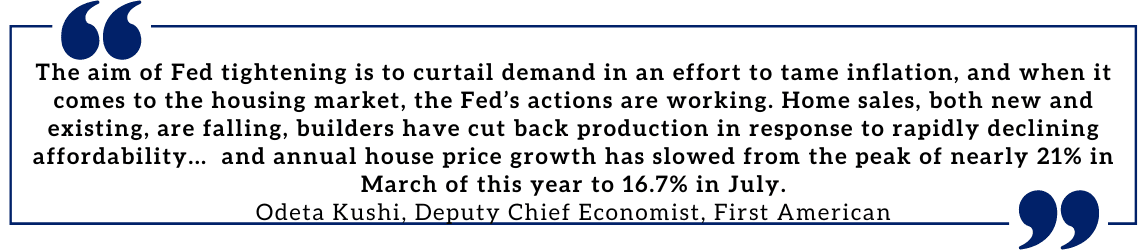

As mortgage rates rise, sales decline. This creates more inventory, or options, in the housing market for buyers as the frenzy of multiple offer situations is behind us. However, as mortgages rates rise, homes are less affordable. One of the best courses of action to combat the affordability issue is to work with a real estate agent who can recommend several, local, trusted lenders to find the right mortgage product for your particular situation. Consider local and national down payment assistance programs.

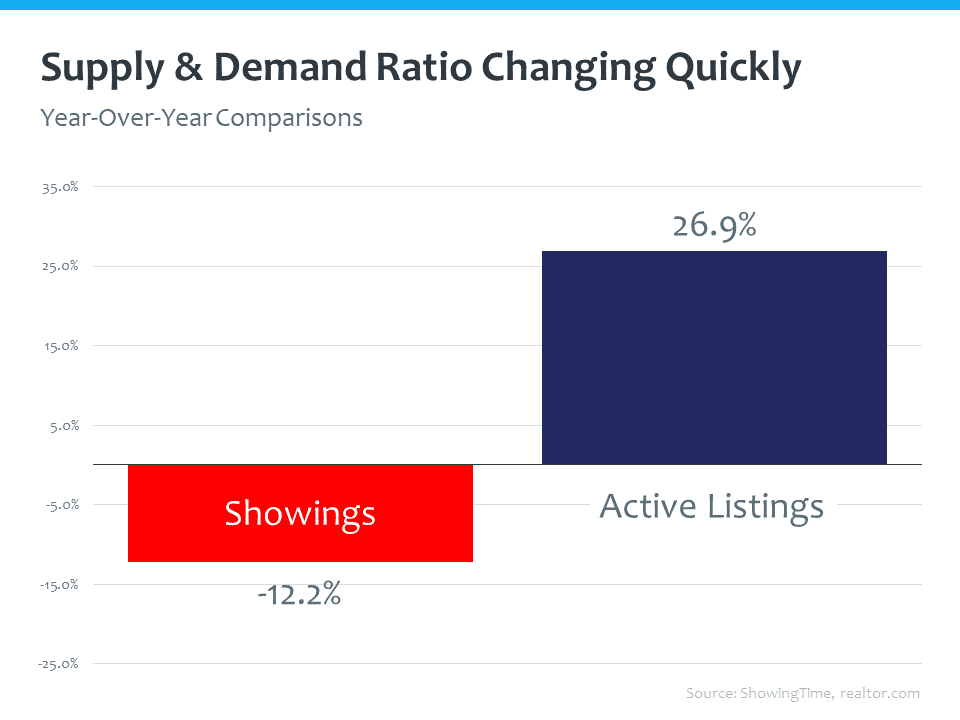

Supply and demand drive prices. The supply and demand ratio has undergone some dramatic changes recently. In real estate, demand is represented by showings, and supply is represented by active listings. The past few years, we saw a real estate market like we've never seen before. For many, the meaning of home changed, for others, interest rates dropped significantly. Whatever the reason, demand was through the roof – lines of people to get into homes, bidding wars, record low inventory, and price escalations. However, today we are seeing a national decrease of 12% in showings and an increase of 27% in active listings.

This is an inflection point in real estate. Prices have to decline to restore market balance.

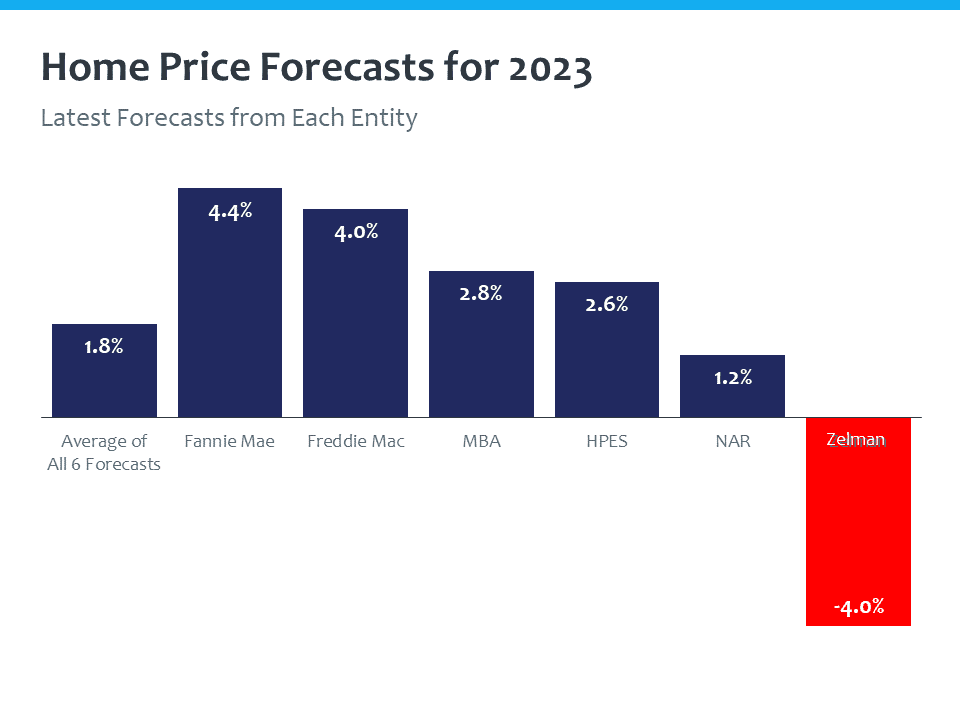

Looking at the 2023 home price forecast of Fannie Mae, Freddie Mac, The Mortgage Bankers Association (MBA), the Home Price Expectations Survey (HPES), the National Association of Realtors® (NAR), and Zelman, we see an average of 1.8% price appreciation.

All this said, many are wondering if now is the right time to buy a home.

Homeownership is truly a long-term financial investment, which means the gains are also long term. Equity is a huge source of wealth creation. The net worth of a homeowner is 40 times greater than that of a renter – a huge differentiator for people's long term wealth gain. Also, the recent record gains in equity are a financial buffer in case economic conditions worsen. Finally, equity is a fuel for housing demand. It is what keeps people in the housing market – what keeps demand high.

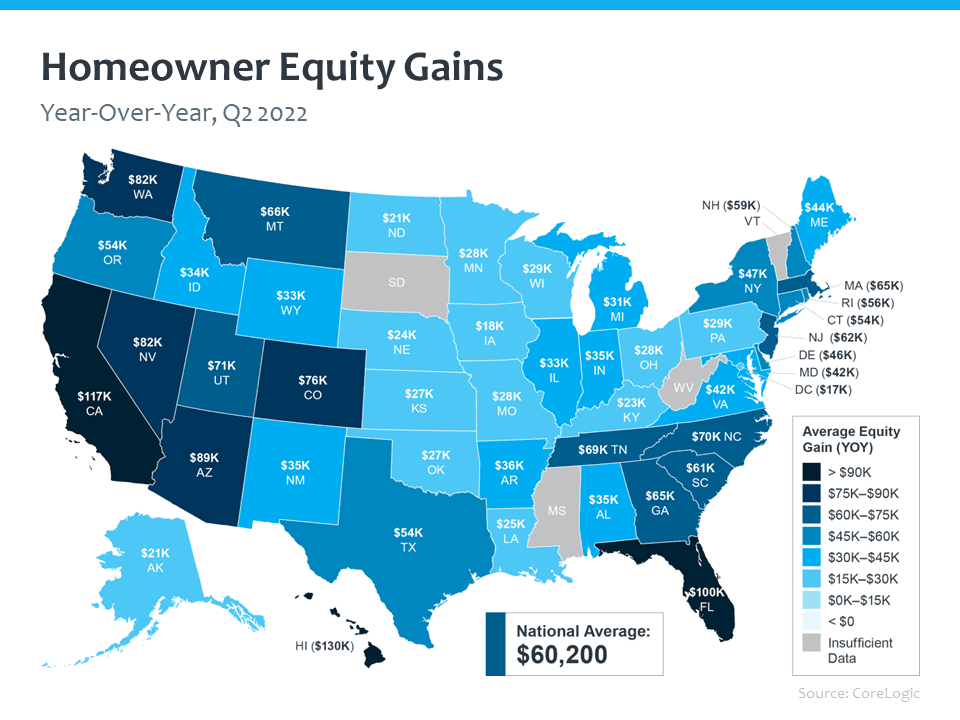

According to CoreLogic, the national average for home equity gain across the country is over $60,000 over the past year, and about $100,000 in Florida. The total average equity per borrower has now reached almost $300,000.

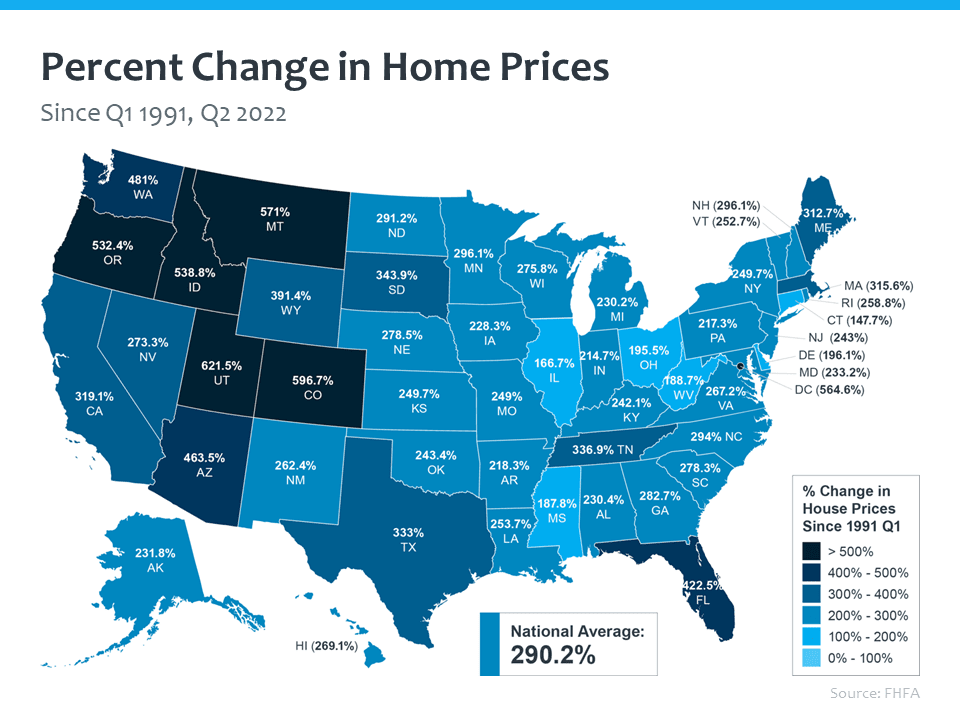

To touch back on the point that homeownership is a long-term game, we take a look at the percent change in home prices over the past 30 years. Home prices have increased by 290% nationally, and over 500% in Florida. That is massive. Throughout all the ups and downs that have happened along the way, home prices are significantly higher.

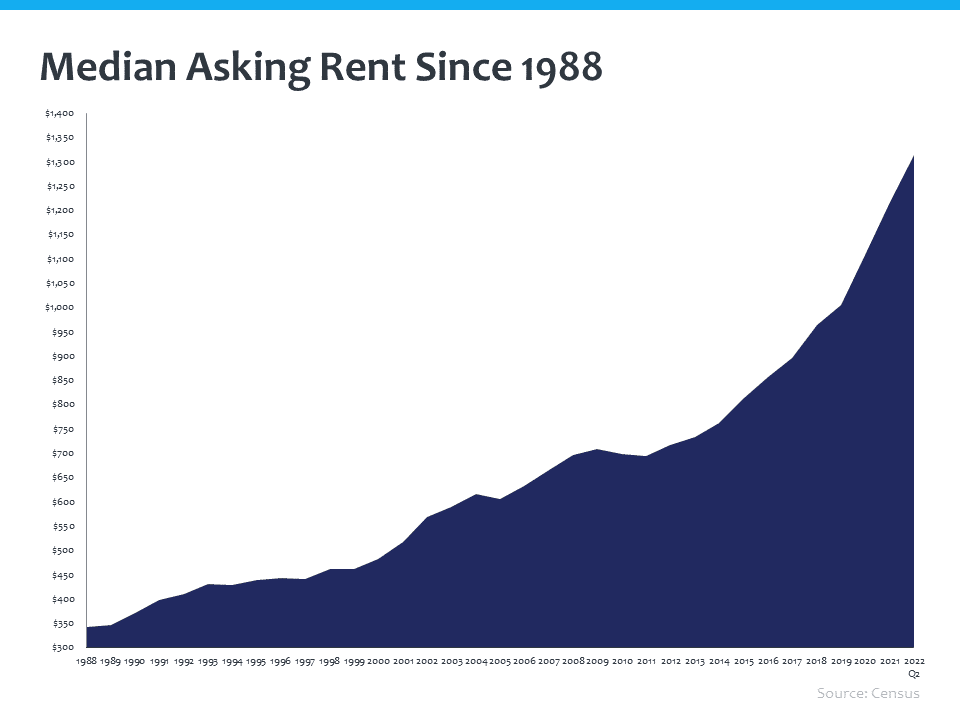

Rent has not only skyrocketed over that same period of time, but provides no return on the investment.

Stay up to date on the latest real estate trends.

All Real Estate News

June 25, 2026

All Real Estate News

June 24, 2026

All Real Estate News

June 23, 2026

All Real Estate News

June 22, 2026

All Real Estate News

June 18, 2026

All Real Estate News

June 17, 2026

You’ve got questions and we can’t wait to answer them.

![We’re not at risk of a collapse today in the financial system like we were before. It’s true - housing may be a little frothy. So housing prices may come down or they may plateau but not to the extent it happened [2008]. John Paulson, Billionaire Hedge Fund Manager Who Called 2008 Crash](https://res.cloudinary.com/luxuryp/images/f_auto,q_auto/azgg7kmr6bqks78rmjeq/6)