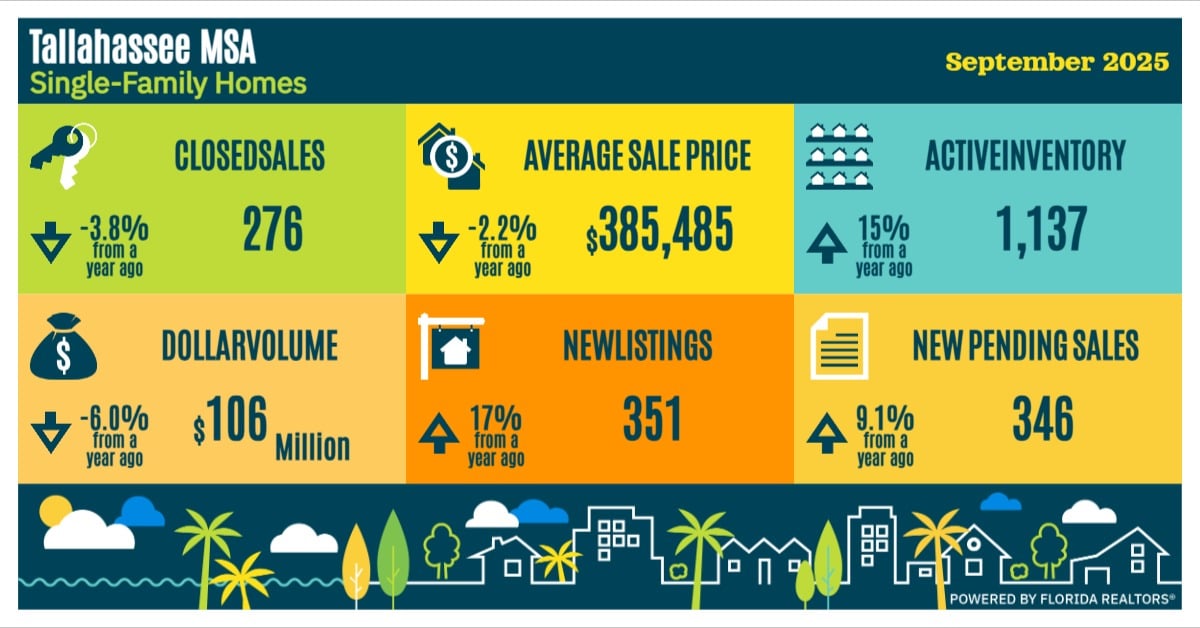

October 2025 Real Estate Market Update

October 14, 2025

Articles for Buyers

October 14, 2025

Articles for Buyers

This month we focus on inventory, home prices, the Federal Reserve, the government shutdown, mortgage rates, home sales, demand, and affordability - for the reminder of the year and into 2026.

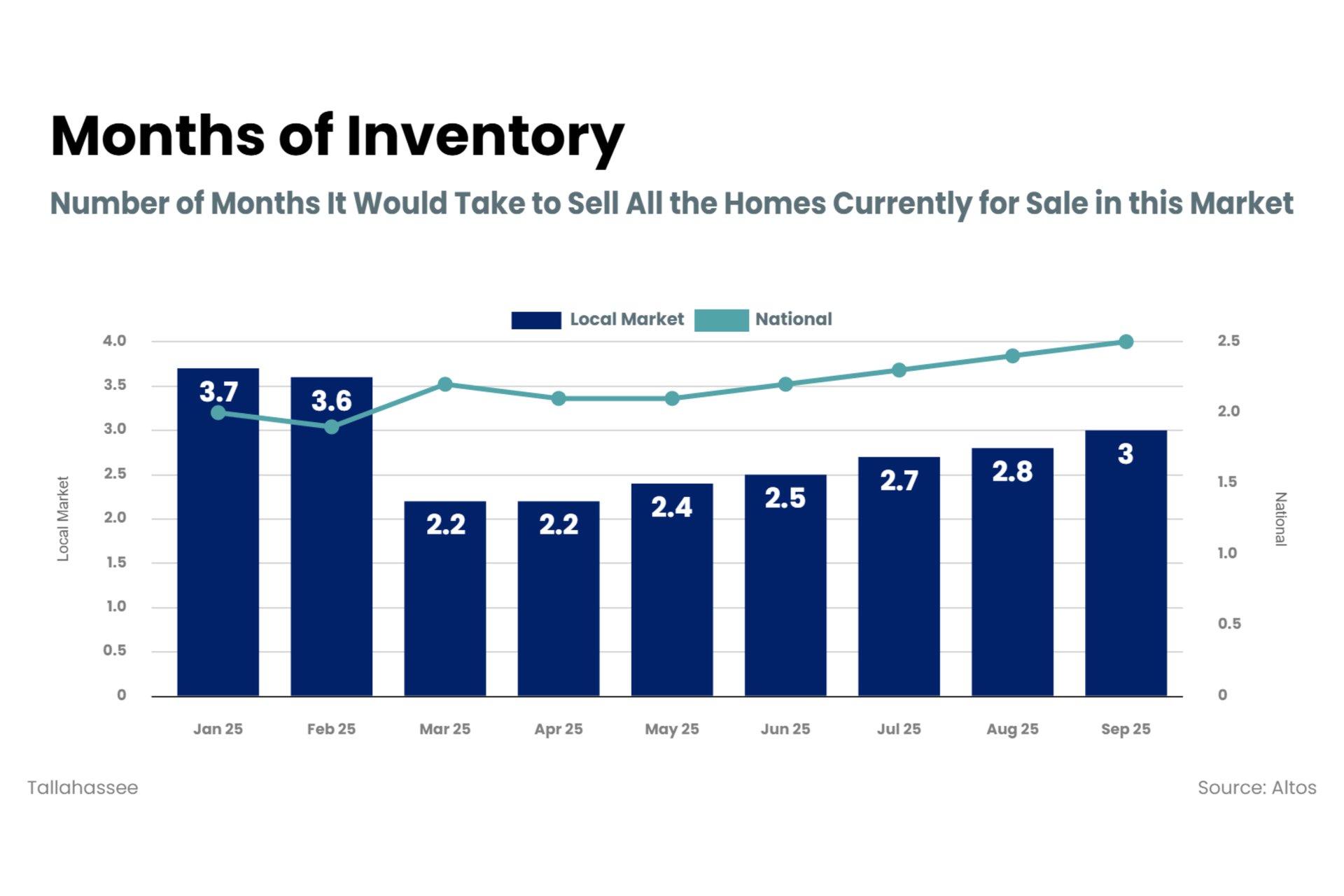

The number of homes on the market continues to rise – both locally and nationally. Increased inventory, every month since May, indicates the dynamic is changing.

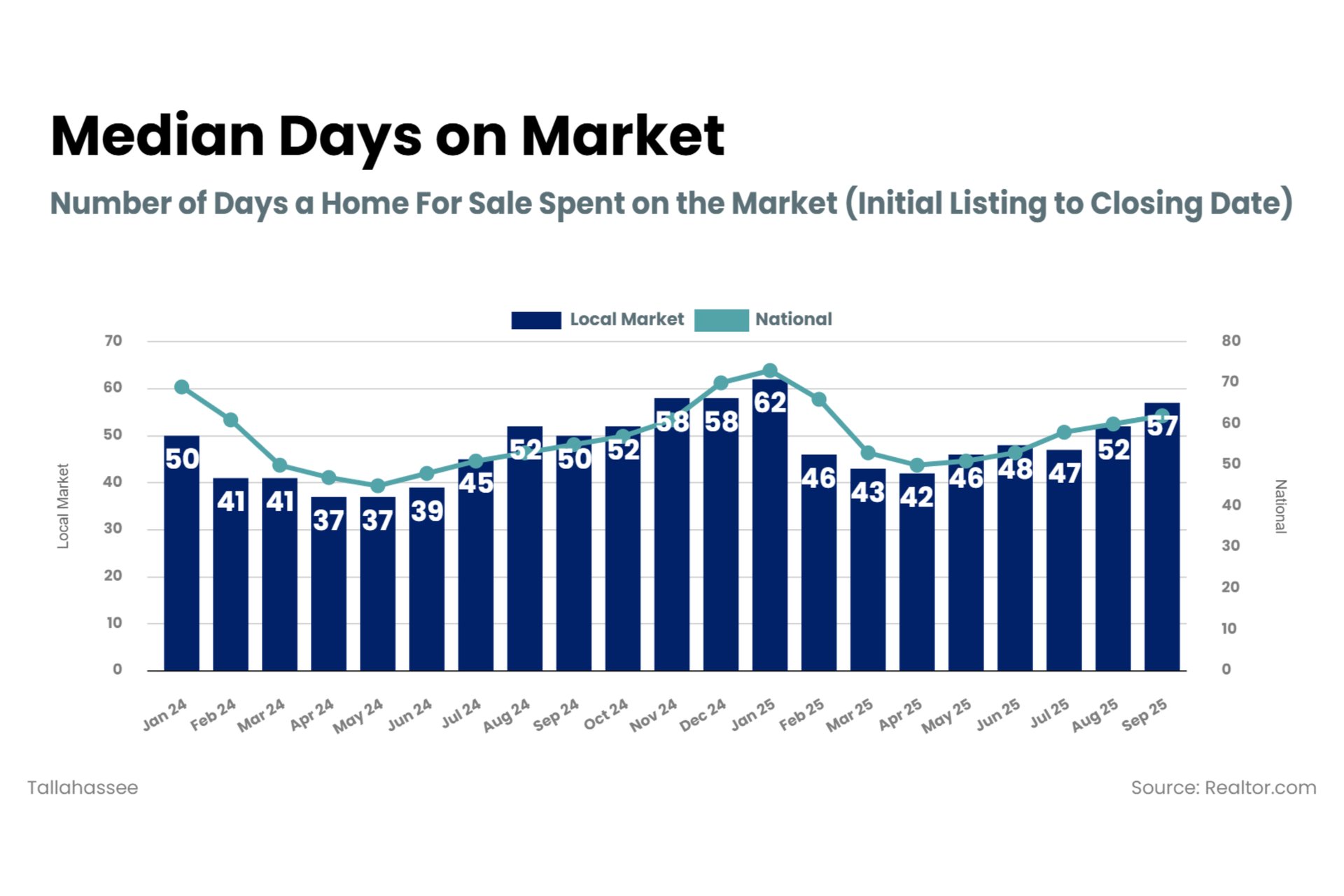

As homes are staying on the market longer, we may begin to see more price reductions as the market shifts.

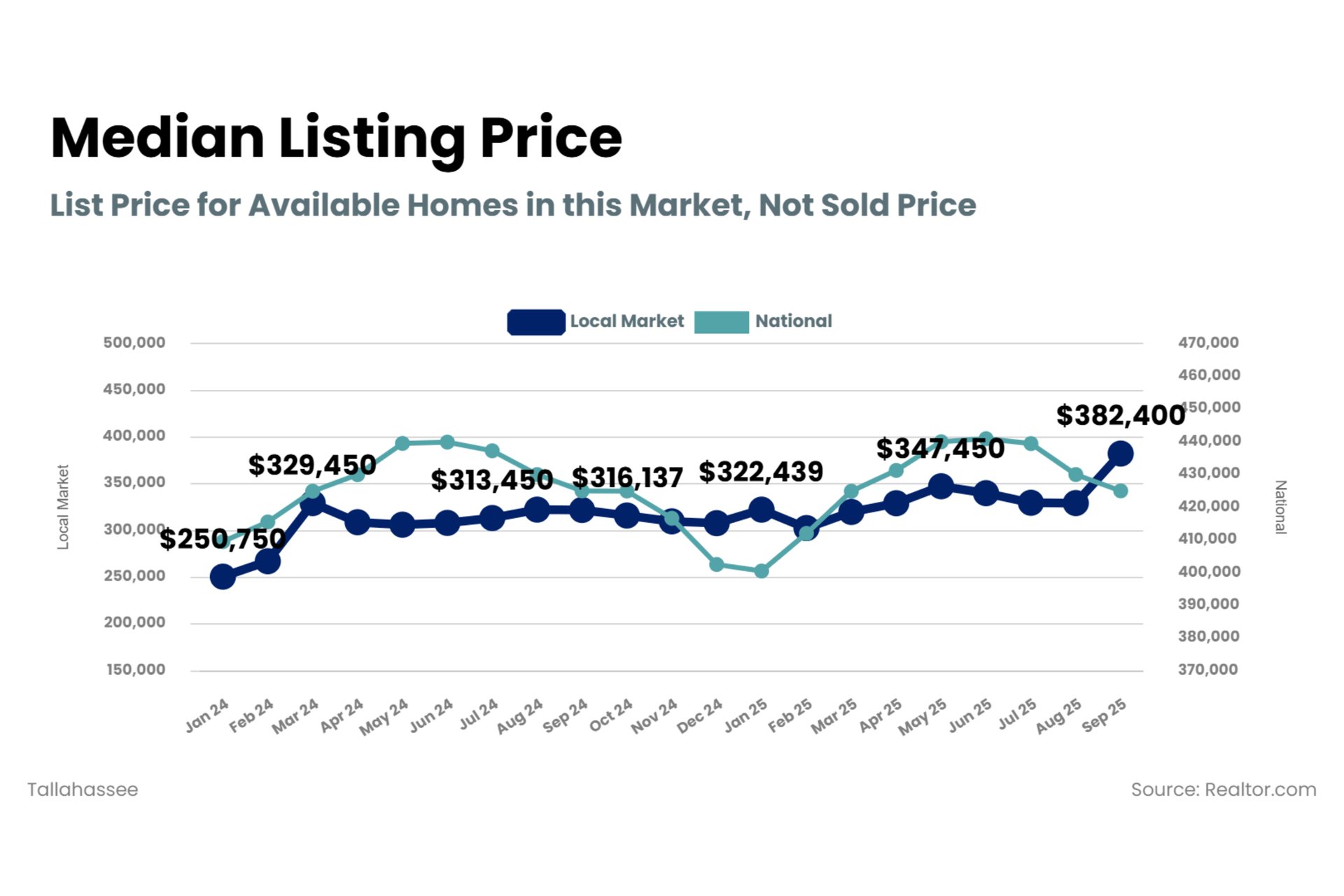

These are all indicators of prices moderating – which they are doing nationally. However, locally, Tallahassee seems to be a bit of an outlier for last month – with an increase in listing prices. It will be interesting to revisit this graphic on next month’s market update to see if we fall back closer to that national trend.

Remember, as we say in most of the monthly market updates: the Federal Reserve does NOT set mortgage rates (we will explain this in the Mortgage Rate Forecast section below). The Fed sets the federal funds rate and what they decide to do (increase, decrease, or hold steady) is a reflection on the broader economy. What they're trying to do is avoid a recession. And what happens in this process is that mortgage rates tend to respond, whether it's leading up to or just after a Federal Reserve meeting.

The Fed has something called a dual mandate. So, there's two things that the Fed is responsible for. First, is price stability - they want to make sure that prices aren't rising exponentially, like they have in years past. Second, they want to make sure that they have maximum employment - they want to make sure that people have jobs. So, they look at a lot of different things to help manage this dual mandate.

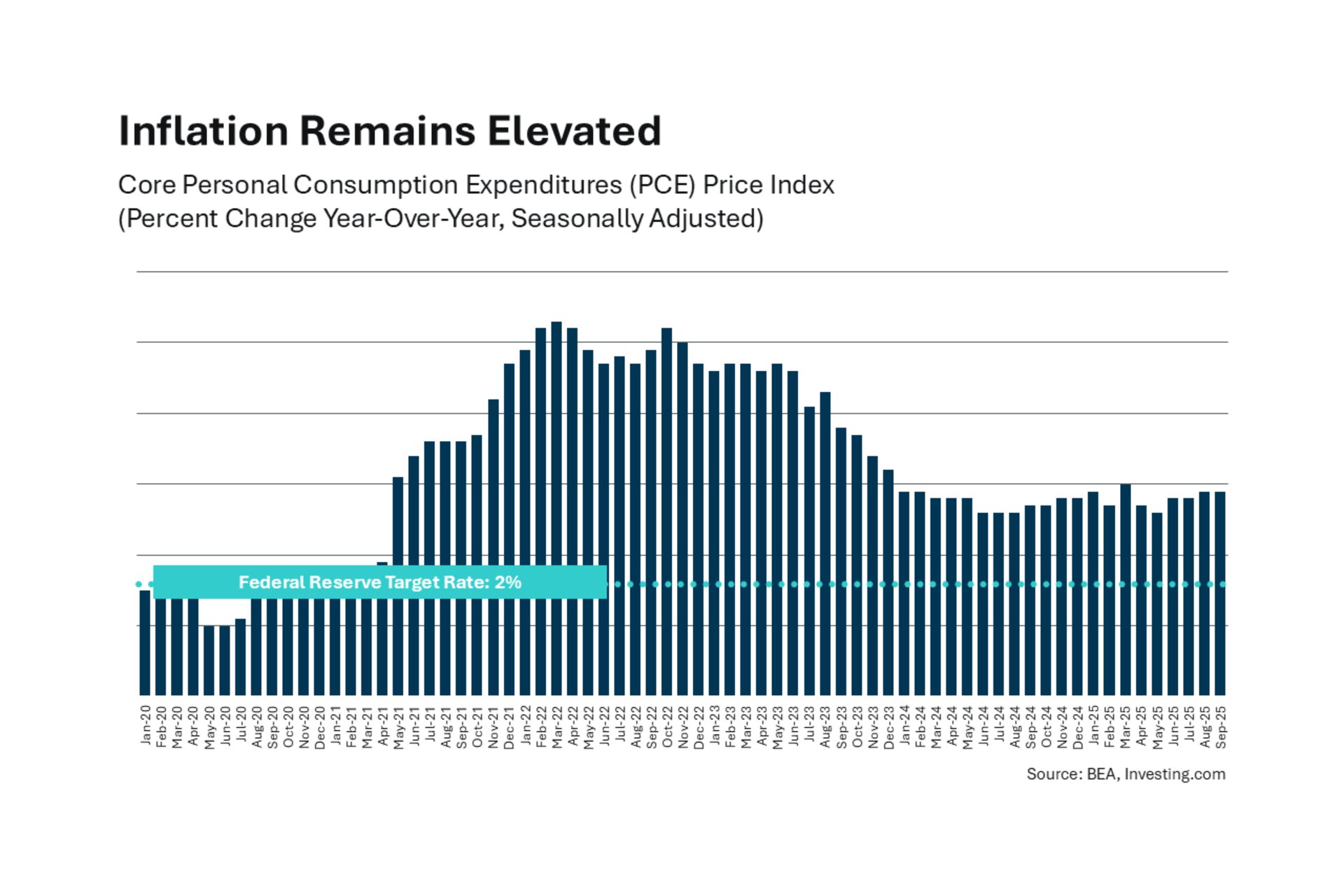

One focus of the Fed is inflation, which remains slightly elevated - a little bit higher than their goal of 2%. However, it is starting to stabilize, and we're seeing that stability over time.

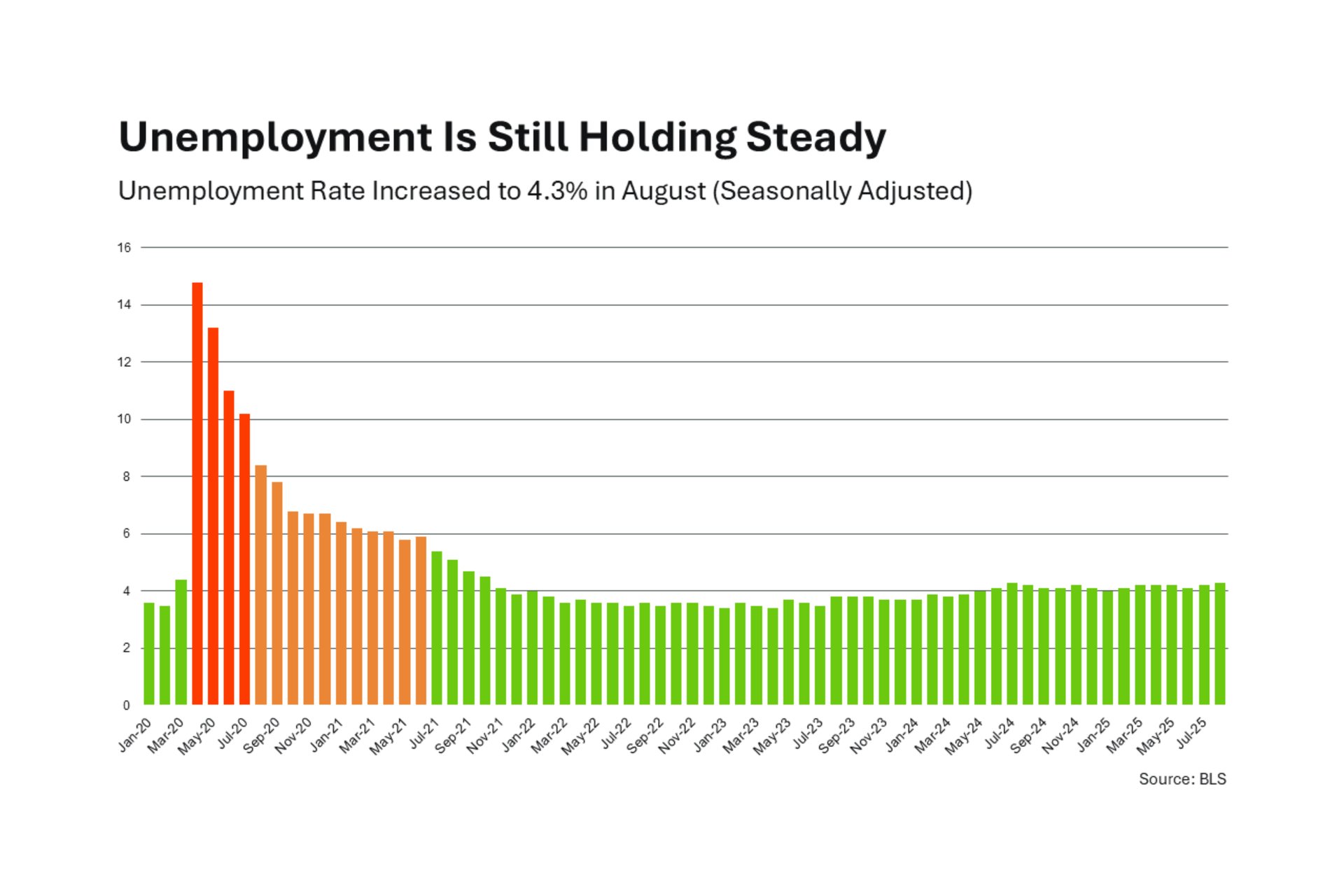

As they aim for maximum employment, they look at the unemployment rate – which is holding steady, but higher than desired.

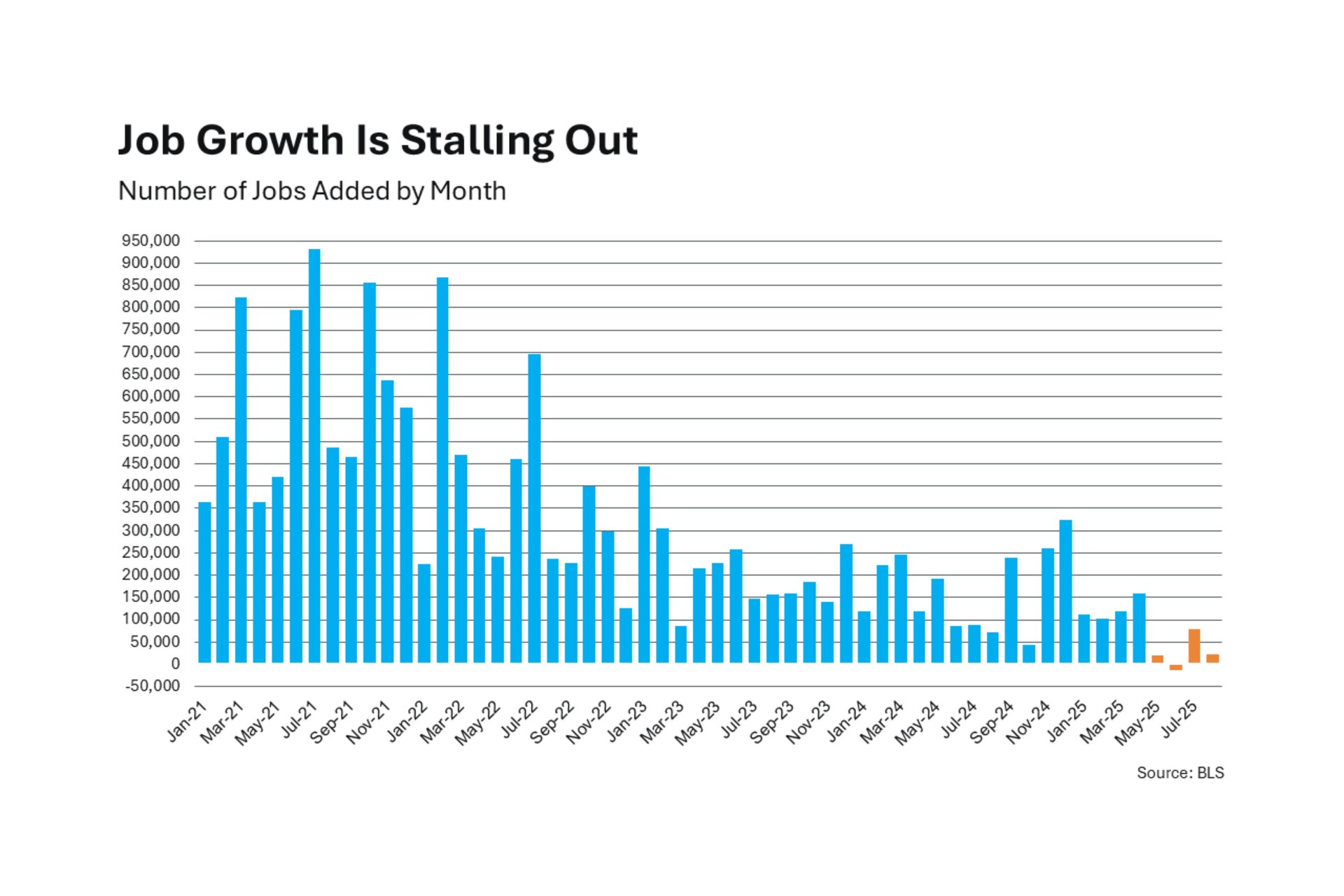

The other thing that can impact the employment side is job growth - which is stalling out because we're not adding as many jobs to the economy right now.

This is the type of data the Fed looks at to make the decisions, and the federal funds rate is a lever they have to impact those figures. What’s interesting right now is that we are in a government shutdown, which could last a couple of days or a couple of weeks. Not knowing when it will end may affect the Fed’s next move, because they can only go off of the information they have.

All this uncertainty affects people’s daily decisions. According to a recent study by LendingTree, 74% of Americans admit that world news and/or current events affect their financial decisions. With this in mind, the future actions of the Fed will be important to keep an eye on.

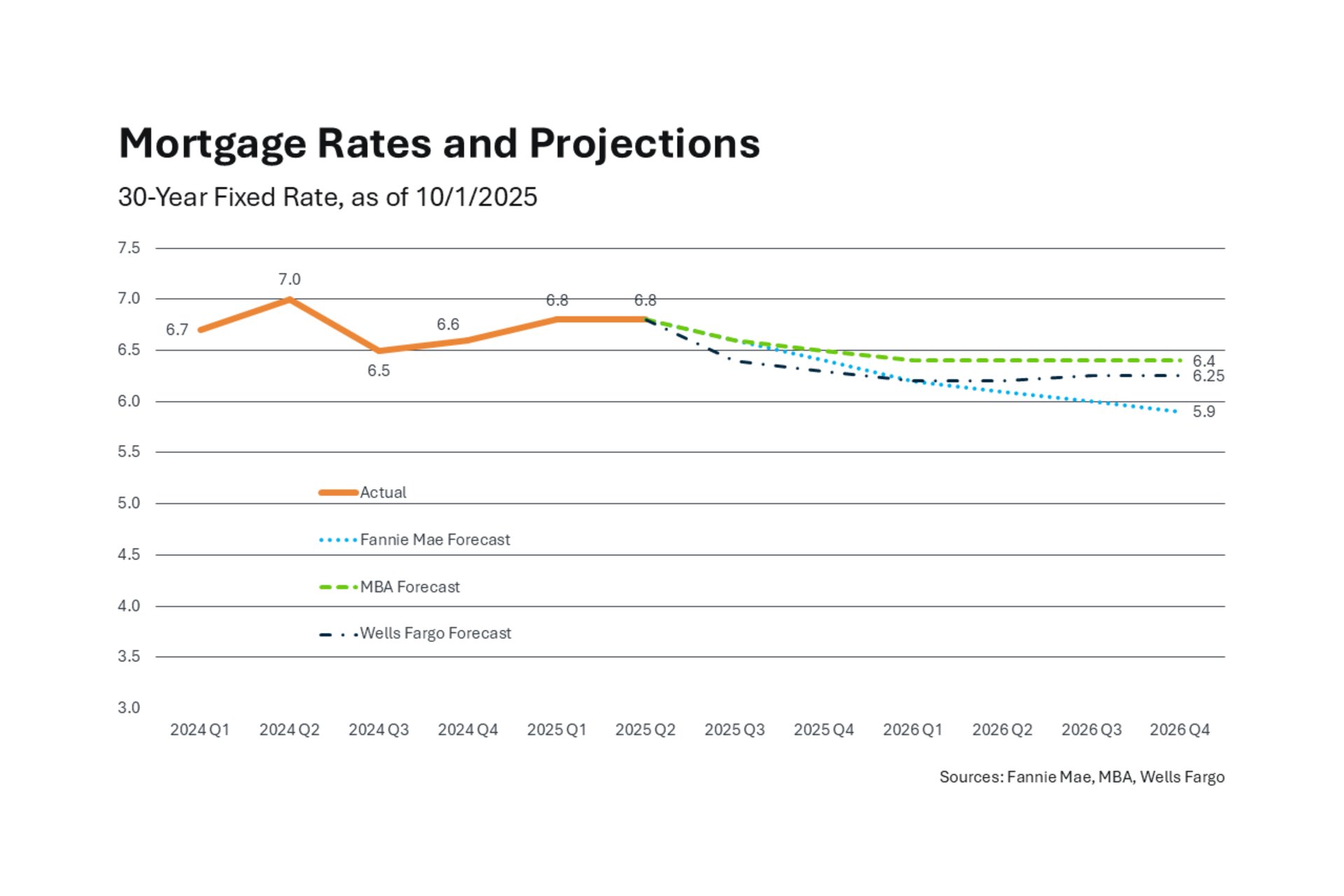

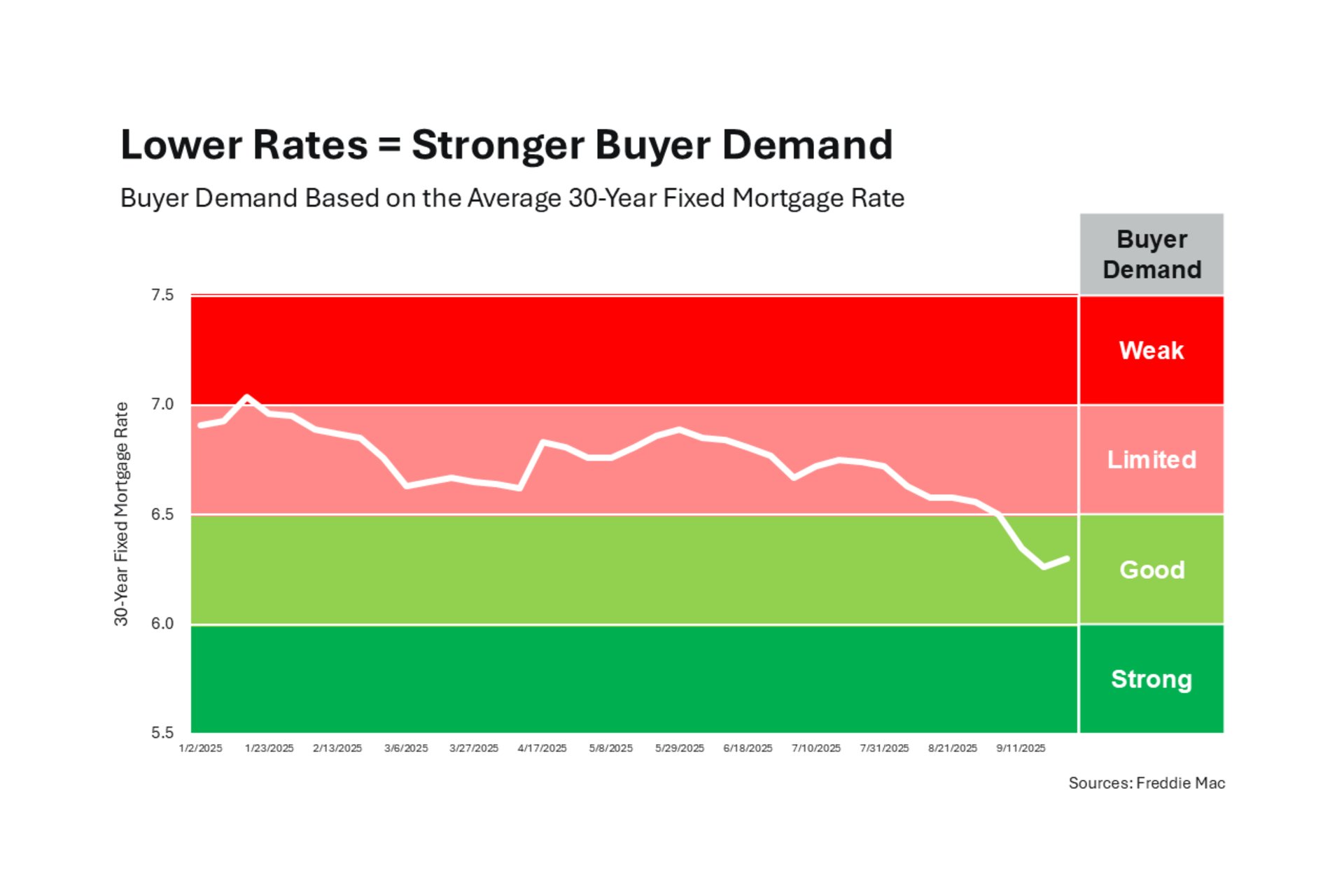

The average mortgage rate projection is in the low 6% range by the end of next year. Based on what we're seeing in the data right now (what's happening in the economy and how the markets tend to react) mortgage rates should come down slightly going into next year. There's going to be some volatility.

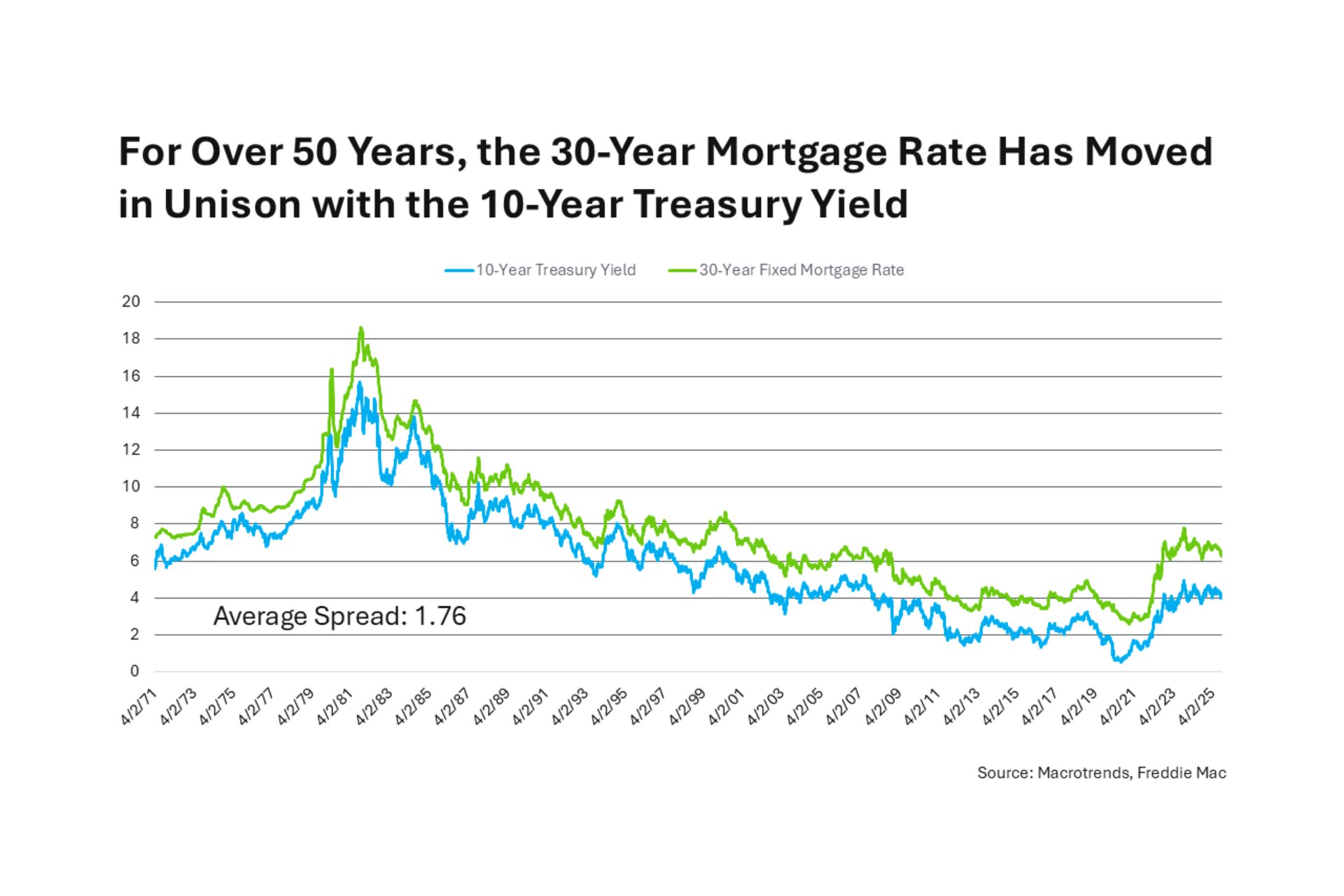

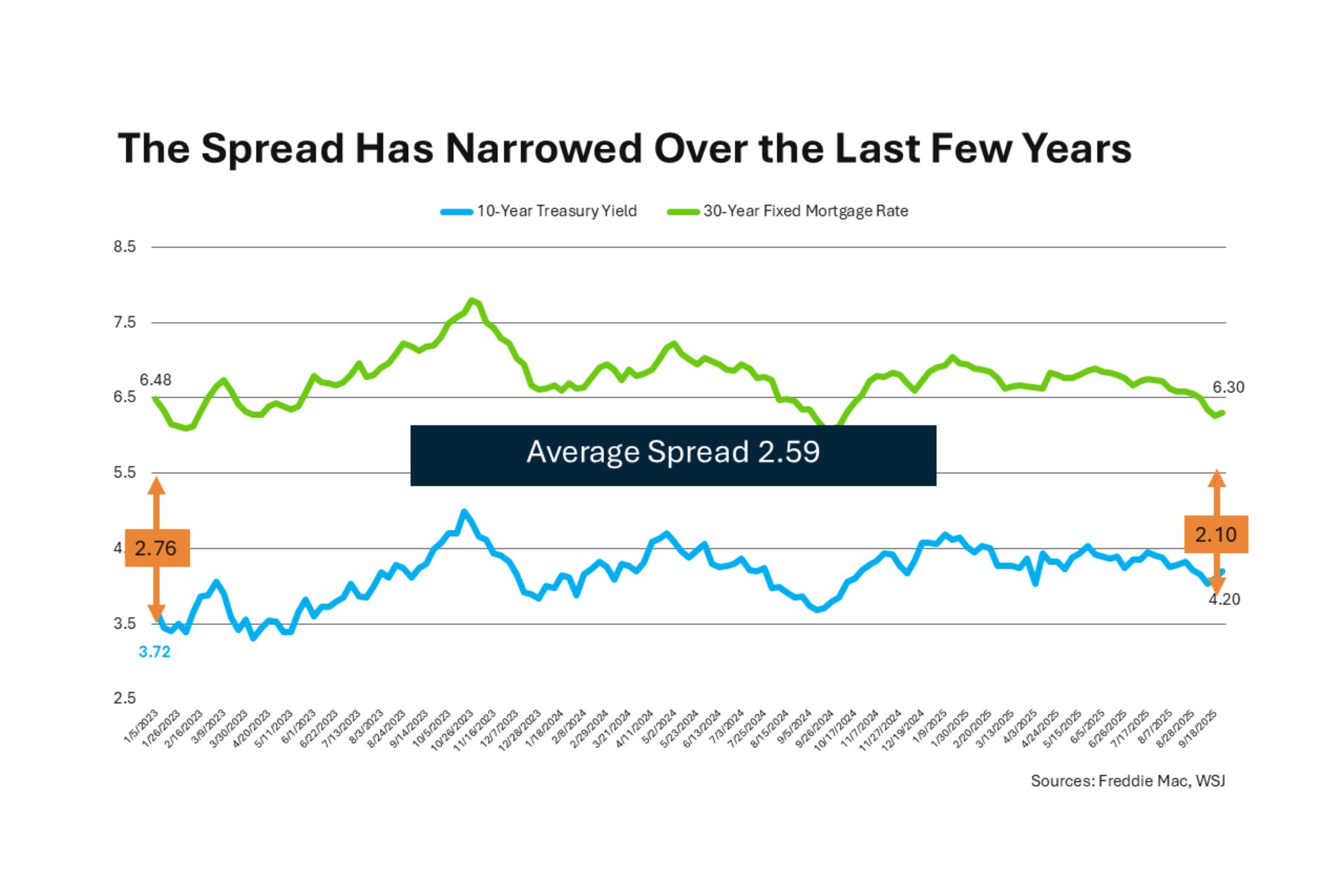

A great indicator of mortgage rates is the 10-year treasury yield. Why? Because for over 50 years, the 10-year treasury yield and the 30-year mortgage rate have moved in unison with each other - when the 10-year treasury goes up, mortgage rates tend to follow, and when it comes down, mortgage rates tend to come down as well. However, there is something called a “spread.” The spread is the difference between the yield and the rate. This difference, historically, averages about 1.76. What this means is that if the 10-year treasury yield is 6.00, then the 30-year mortgage rate is about 7.76 (1.76%, or 176 basis points, higher). It is sort of a symbiotic relationship.

That said, something different has been happening over the past few years: That spread increased from 1.76% to 2.59%. It can be said that this gap represents fear in the market – the larger the gap, the more uncertainty. But, the gap is starting to narrow, which is not only a good sign, but likely why mortgage rates are trending down. Lower mortgage rates mean better affordability. It is important to note that all forecasts do point to a very gradual decline, so don’t expect anything drastic – especially in such a volatile economy right now.

In real estate, when mortgage rates go down, demand picks up, and activity rises. Right now, we are seeing good demand, which may become more strained if we move back towards a 6.5% mortgage rate. And, as demand increases, so do prices.

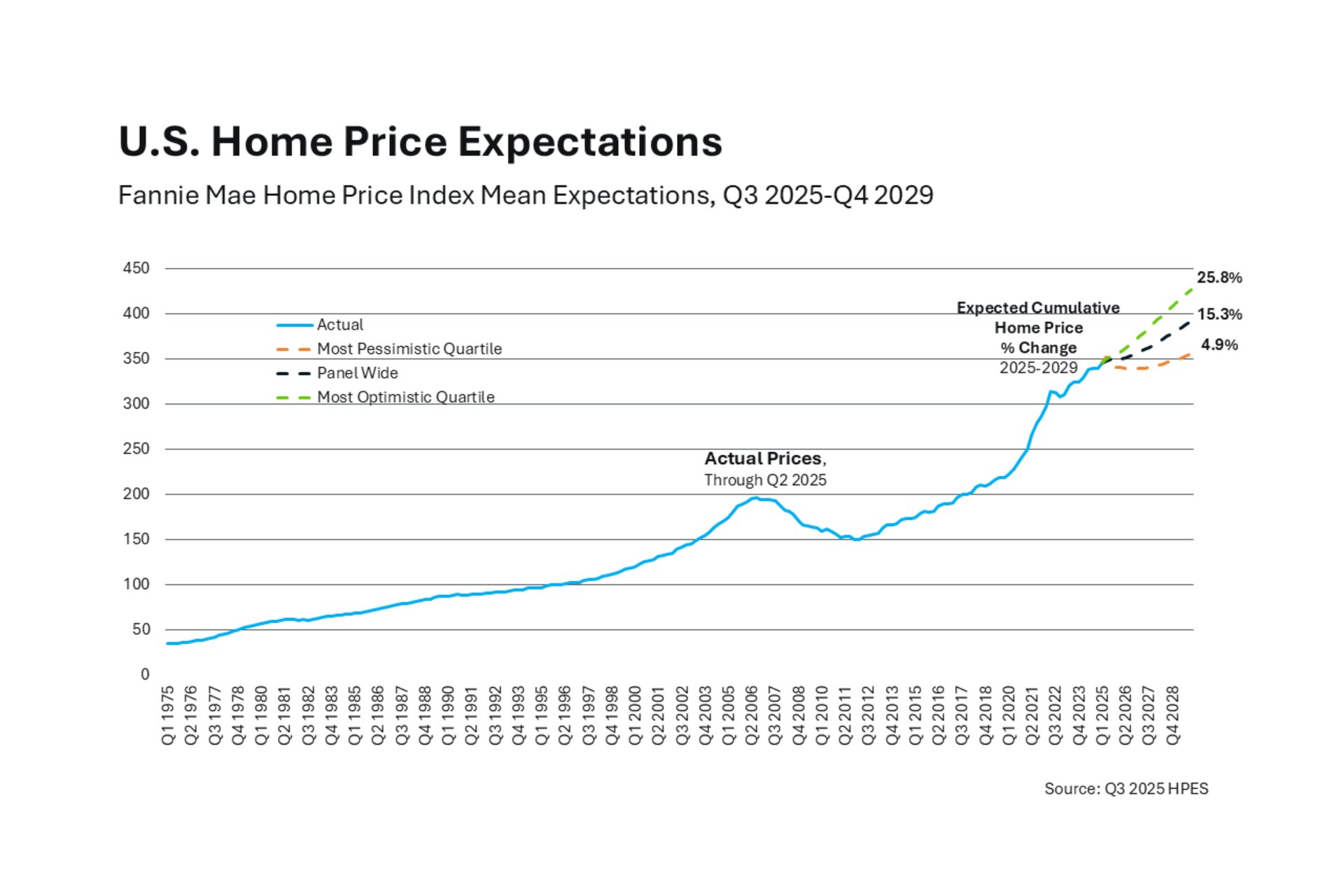

The U.S. Home Price Expectation Surveys is made up of about 100 economists and industry experts who look at the data available and project out what they think home prices are going to look like over the next 5 years. The optimists are saying home prices could rise nationally by about 25% over the next 5 years, but the average is closer to 15%. What's interesting is even the pessimists, the people who are on the much lower end of the scale when it comes to home price projections, are saying there will be growth over the next 5 years – at a much more moderate, much more sustainable, much healthier pace for the market than we saw a few years ago. That's definitely another good sign for the stability of the housing market.

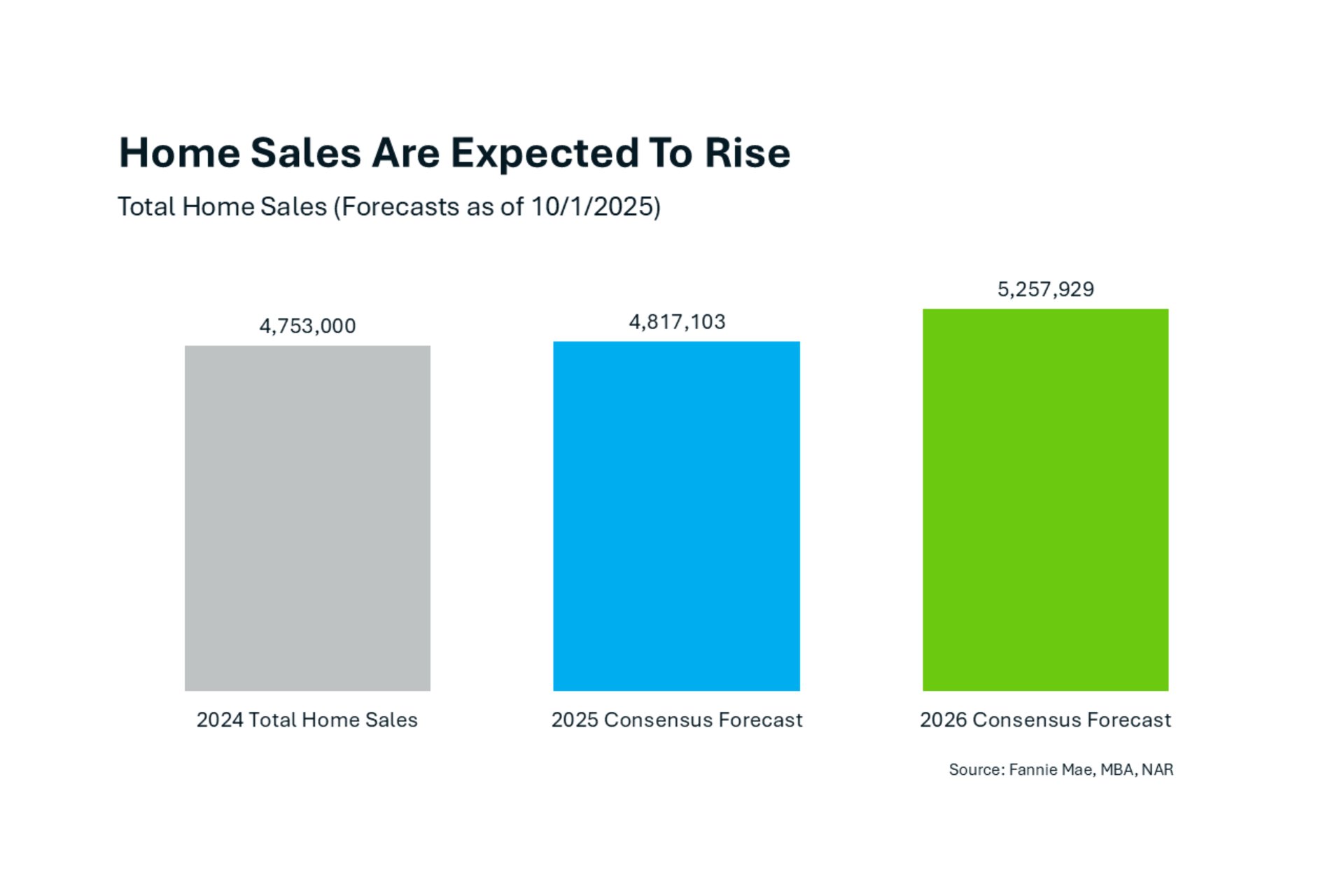

So, with home price growth expected to continue, and mortgage rates expected to go down, what does that mean for home sales?

Well, we're expected to end this year with more home sales than last year, and 2026 is expected to see even more homes sell - that's existing homes, plus new homes. Now, it’s not a huge jump, but it is good news. The combination of more inventory, higher demand, easing mortgage rates, moderating home prices, and improved affordability will be the wind at the back of the real estate industry as we close out the year and head into 2026.

· Inventory is increasing, causing homes to sit on the market longer, which is causing home prices to moderate – signaling a shift in the market.

· All eyes are on the Federal Reserve’s next move, especially in light of the government shutdown.

· Mortgage rates are expected to ease.

· Home prices and home sales are both expected to increase.

· The combination of more inventory, higher demand, easing mortgage rates, moderating home prices, and improved affordability will be the wind at the back of the real estate industry as we end 2025 and head into next year.

Stay up to date on the latest real estate trends.

All Real Estate News

July 27, 2026

All Real Estate News

July 23, 2026

All Real Estate News

July 22, 2026

Articles for Sellers

July 21, 2026

All Real Estate News

July 20, 2026

All Real Estate News

July 16, 2026

You’ve got questions and we can’t wait to answer them.