April 2023 Real Estate Market Update

April 17, 2023

All Real Estate News

April 17, 2023

All Real Estate News

The demand-based rate environment we are in today is good – with economic changes having a positive effect on mortgage rates.

It seems the turbulence in the secondary and banking markets is putting a downward pressure on mortgage rates, and as rates come down, it makes homes more affordable. However, mortgage rates aren’t the only thing that affect affordability. Wages and home prices are the two other factors that play into the affordability equation. We know wages have increased, so let’s take a look at home prices.

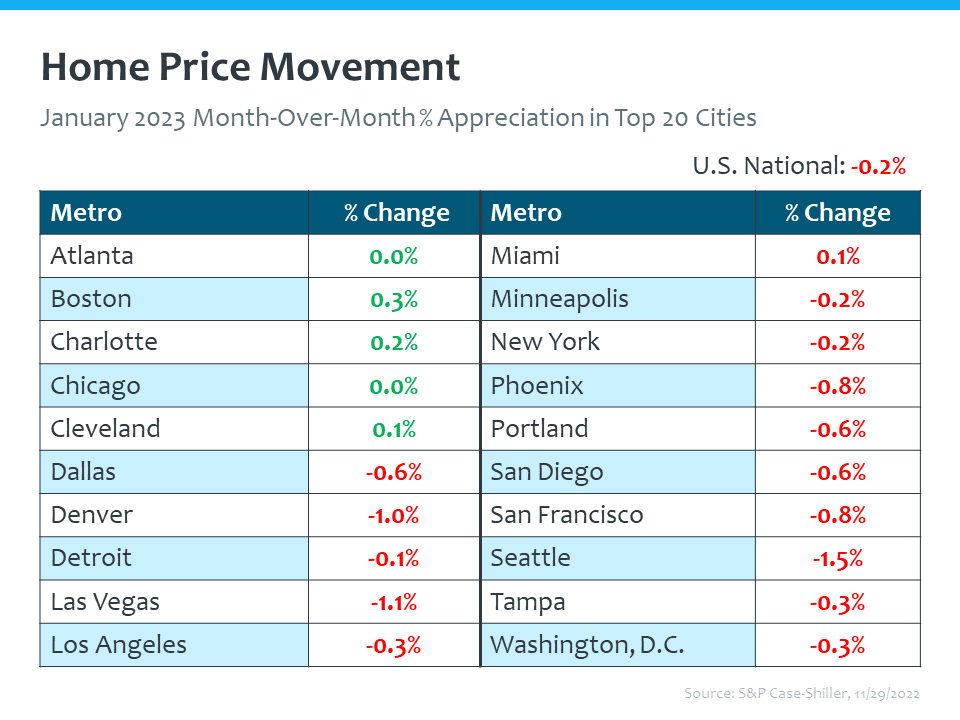

Nationally, home prices have appreciated 3.8% over the last year. Case-Shiller breaks down this appreciation in the top 20 cities, where the West Coast does seem to see some depreciation, while Florida cities are reporting the highest appreciation.

The Federal Housing Finance Agency reports a national rate of appreciation of 5.3% with the Pacific flat year-over-year, and the South Atlantic at 9.6%.

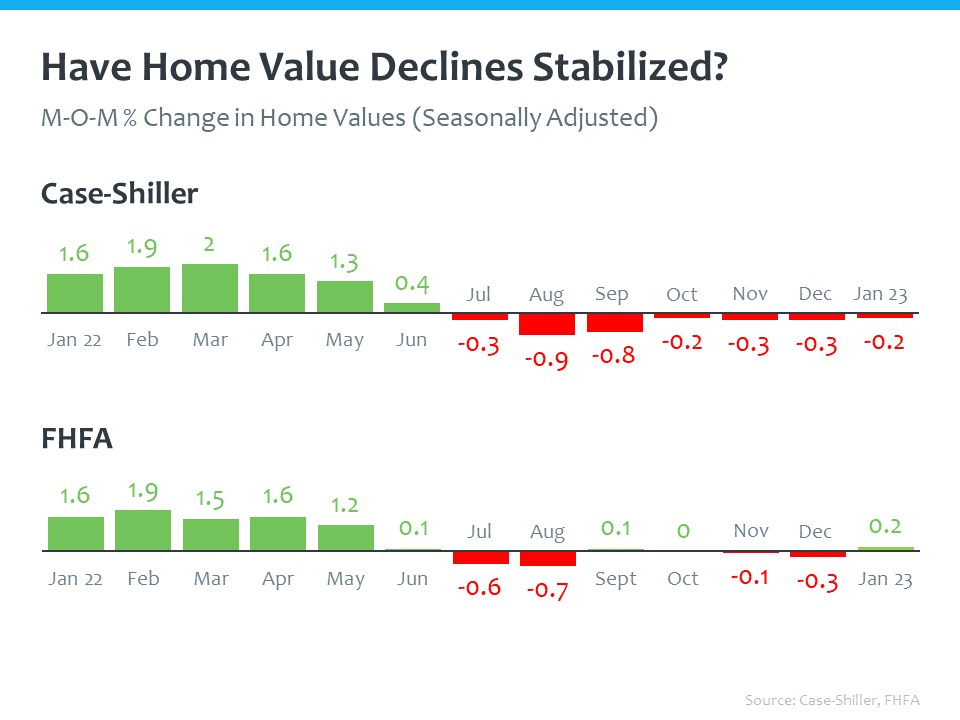

However, if we were to look at the month-over-month data on pricing, the situation is a little bit different. According to Case-Shiller, we are seeing slight depreciation month-over-month. This is not a runaway scenario of depreciation, but depreciation none the less. Nationally, -0.2% depreciation overall.

The Federal Housing Finance Agency shows a national average of 0.2% appreciation. Overall, it seems the worst depreciation is behind us.

Charting out both Case-Shiller and the Federal Housing Finance Agency data for home values month-over-month going back to January of last year, we can see that depreciation peaked in the fall and has stabilized. Prices are not in a free fall.

Overall, affordability is historically low, according to the National Association of Realtors. In January of last year, it was more affordable to buy a home before rates more than doubled. Throughout the year, we saw affordability decline, and now we see it moving in the right direction. The dotted line is the threshold on the index (a score of 100). This threshold represents a home buyer making a median income being able to afford a median priced home. In other words, a score of over 100 means that homes are more affordable, and today we sit at 104.9.

When it comes to affordability, monthly mortgage payments is what it all boils down to for the buyer. The median monthly mortgage payment, peaked around October of last year, according to the National Association of Realtors – down about $200 since last October.

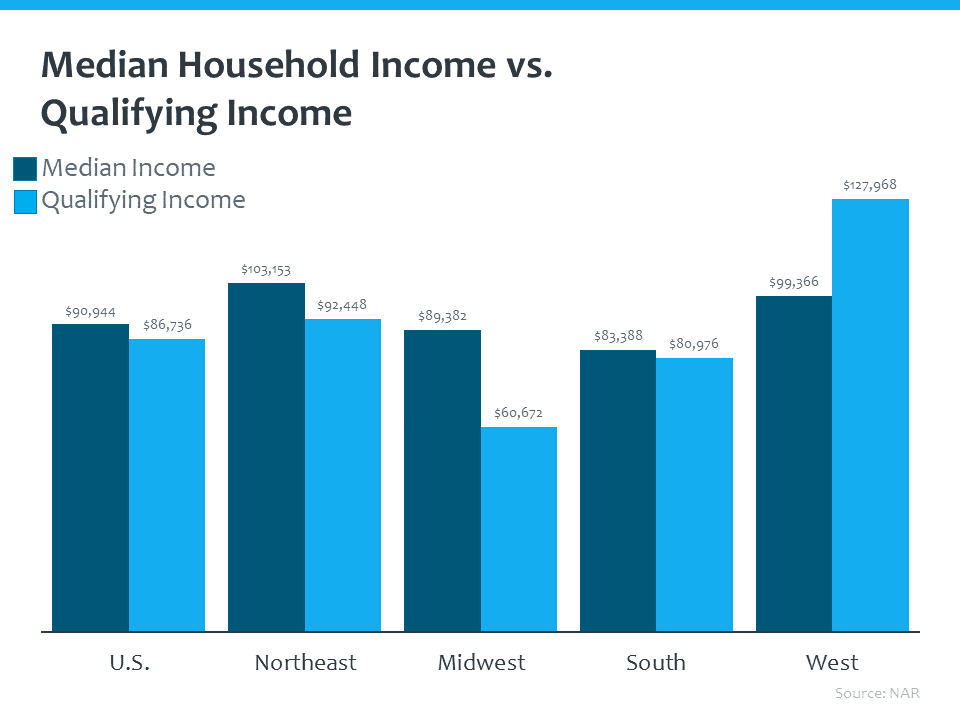

When discussing monthly mortgage payments, we would want to consider median household income versus qualifying income for a median priced home. According to the National Association of Realtors, it is much more expensive to purchase a home on the West Coast than it is in some of the other markets. So, on the West Coast individuals are not making the income that it takes to qualify for a median priced home. It’s the opposite in the Northeast, Midwest, and South. In these regions, those making a median income should be able to qualify for a mortgage on a median priced home.

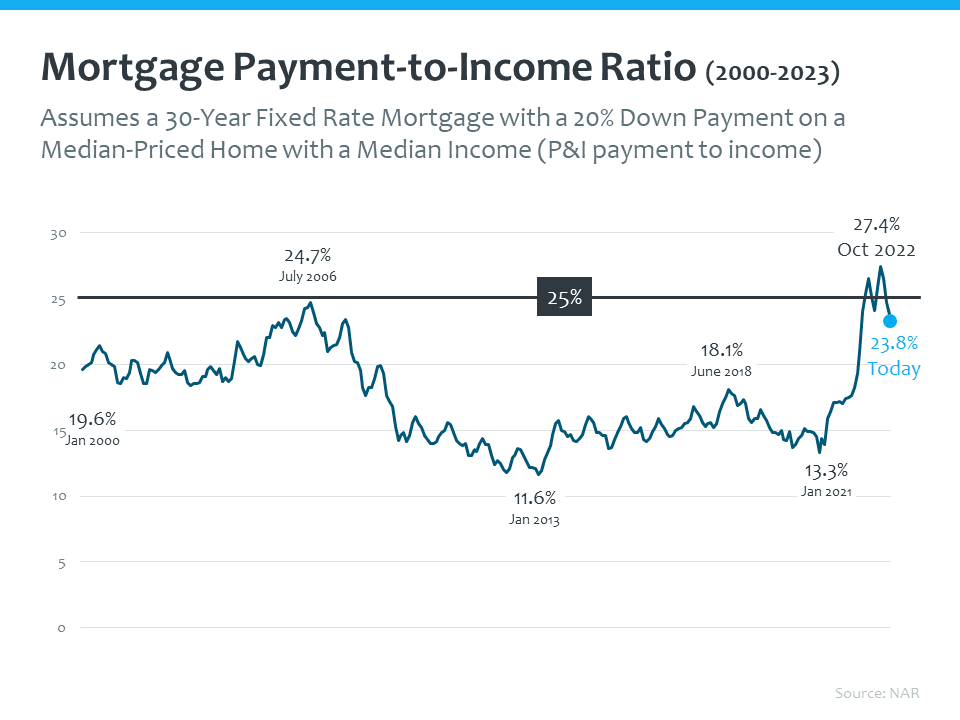

It is recommended by the National Association of Realtors, that no more than 25% of a household’s income should be spent on principle and interest. Looking as far back as January of 2000, we were under that 25% threshold for a long time. While we saw a historic high of 27.4% in October, we sit below the threshold now at 23.8%. Affordability is moving in the right direction.

Stay up to date on the latest real estate trends.

All Real Estate News

June 23, 2026

All Real Estate News

June 22, 2026

All Real Estate News

June 18, 2026

All Real Estate News

June 17, 2026

All Real Estate News

June 16, 2026

All Real Estate News

June 15, 2026

You’ve got questions and we can’t wait to answer them.