As we take a look at the interest rates since January, we can see that is what is really defining the current real estate market right now and the volatility is a result of the moves the Federal Reserve is making to ease inflation – the enemy of long-term interest rates.

The National Bureau of Economic Research defines what a recession is and when it is. A recession is a significant decline in economic activity, spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale retail sales. Technically, a recession is 2 consecutive quarters of negative growth.

Looking all the way back to the 1940s, every time we’ve seen two consecutive quarters of negative growth, a recession has been called.

According to a survey from the Wall Street Journal that asked economists if they believe a recession will happen in the next 12 months, we can see more and more of the experts are predicting a recession. A recession is an economic slowdown where, historically, we have seen homes appreciate in value and mortgage rates fall.

In 4 of the last 6 recessions, home prices actually appreciated in value, except for 2008, which we have covered in previous monthly market updates was a fundamentally different place than where we are today.

In all 6 of the last 6 recessions, interest rates have declined.

One of the biggest reasons a housing crash is not predicted is inventory. In 2008, we had an oversupply of homes on the market – which causes home prices to fall. Today, we have an under supply – which causes home prices to rise.

We are seeing about a 3-month supply of homes (inventory). We are far, far away from the 10-month supply of homes we saw leading up to and in 2008. The typical neutral market is 6 to 7 months of supply of inventory.

Inventory can also come from new construction. Building permits and housing starts are the leading indicators (what is to come), while under construction and housing units completed are the lagging indicators (what has happened). The leading indicators are slowing down from May to June as builders are seeing mortgage rates rise. This shows further confirmation that we’re not on pace to have an oversupply.

Finally, inventory could come from distressed properties like foreclosures and short sales. The mortgage credit availability index shows how much harder it has become for someone to secure a home loan as lending standards have tightened. More qualified buyers means less distressed properties.

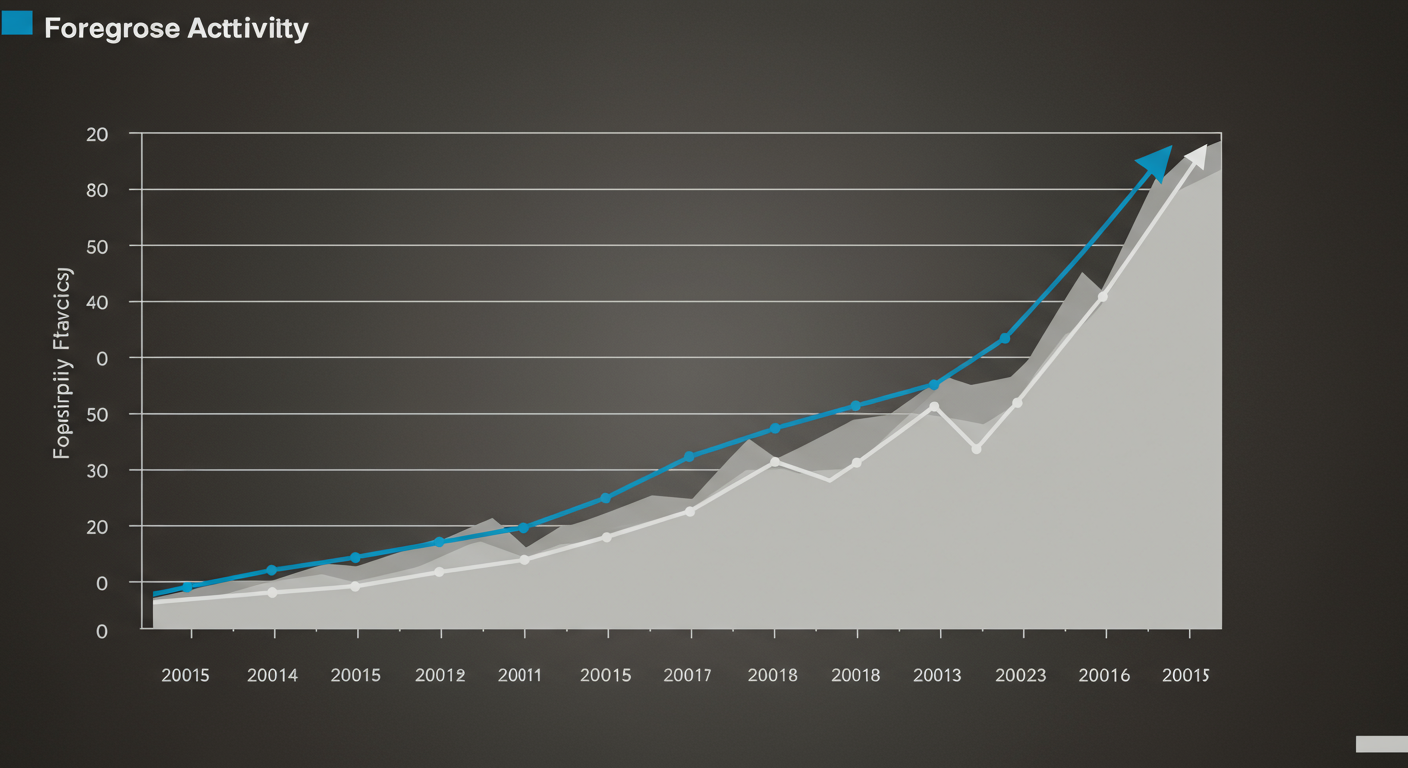

There are fewer and fewer foreclosures every year in this country, and especially in the past year or two due to the moratorium on foreclosures.

Looking at foreclosure activity by year, going back to 2008, we are seeing about half of the foreclosures compared to pre-pandemic numbers and less than 10% of post-2008 numbers. Lending standards have changed the game.

36% of mortgages coming out of forbearance were paid off. 45% worked out repayment plans (modifications, loan deferrals, etc) – an opportunity that homeowners didn’t have in 2008. The forbearance program changed the game. 4 out of 5 homeowners are coming out of forbearance. However, 17% have no loss mitigation plan, but mostly have enough equity to be able to sell their homes and avoid the foreclosure process. Today, there are different options, and why we won’t see a wave of foreclosures coming to the market. If all 400,000 homes in forbearance came to market, it would still be under supplied.

The increased amount of foreclosures this year could be due to the lack of foreclosures the past two years.

Today, we are in a seller’s market, but what does the rest of the year hold?

Freddie Mac, Fannie Mae, the Mortgage Bankers Association, and the National Association of Realtors® are predicting mortgage rates to waiver around the current rate with a more stabilized rate next year.

Looking at what the 7 key industry leaders are saying about home pricing, we are seeing about 10.3% home price appreciation through the end of this year. A more moderate growth than the 15% we saw last year, but still extremely healthy appreciation in most markets.

There is also a decrease in home sales due to the softening of buyer demand in light of the rising mortgage rates. The National Association of Realtors® is saying that, at the current pace of sale today, we are projected to sell 5.1 million homes in this country this year. Of course, that is a decrease considering the sales the past 2 years, which were extraordinary years in the real estate market. The 5.1 million projection puts us back in line with the pre-pandemic years of 2017-2019.

In lieu of the rising mortgage rates, Freddie Mac, Fannie Mae, and the Mortgage Bankers Association re-forecasted their home sales predictions for 2022 from 7 million to 6 million. Still a very strong number, which should hold steady as the interest rates begin to balance out.

Today there are fewer multiple offer scenarios, fewer homes selling above asking price, and the supply of homes for sale is growing – all providing a great scenario for buyers right now. We have dropped from 5.5 offers on a home in April to 3.4 in June. We’ve gone from 61% of homes selling above asking price to 51% – still competitive, but decreasing. Finally, inventory has creeped from 2.2 months supply on hand to 3.0. All three trends that should continue moving forward.