February 2020 Real Estate Market Update

June 9, 2020

All Real Estate News

June 9, 2020

All Real Estate News

The above image shows the percentage of the Wall Street Journal’s Survey of Economists, and their belief in when a recession will take place. Back in 2018, 67% of the economists thought the recession would occur by the end of this year. Just this past October, only 34.2% had the same thought. And, just a month or two ago, we see that now only 14.3% of economists believe the recession will occur by the end of this year.

We are in the largest economic recovery in the history of the United States. Interestingly enough, one of the reasons the timeline is being pushed back is because the housing industry is doing as well as it is.

Here is some information from Showing Time’s latest Buyer Traffic Report. Year-over-year buyer activity has increased substantially, and it’s increased in every single region. We are all seeing more buyer traffic in this year than we did the same time last year. That has also been confirmed by the National Association of Realtors (NAR). Two-thirds of the country is seeing double digit increases here.

We saw 2019 come to a close with the economy churning out 2.3 million jobs, mortgage rates below 4%, and housing starts ramp up to 1.6 million on an annual basis. If these factors are sustained in 2020, we will see a notable pickup in home sales in 2020.

Lawrence Yun, Chief Economist at NAR

The housing market is very vibrant right now. Essentially, people want to buy houses. Across the country, buyer activity is very strong. However, when we go to selling traffic, we see that dies off pretty dramatically. So, the amount of people looking to purchase a house is increasing dramatically, but the amount of people ready to sell their house isn’t reaching the same levels.

The market is struggling with a large housing undersupply. The number of homes for sales are poised to reach historically low levels.

George Ratiu, Senior Economist at realtor.com

George Ratiu made the comment above weeks ago, and the new numbers are in! The number of homes for sale is at 1.4 million. That number was last seen in 1993. The month’s supply of inventory dropped to 3.0 months. People who have been in this business for almost 30 years have never seen inventory at 3.0 months.

Well, it’s December. It’s the time of year where a lot of people take the house off the market.” He said, “Inventory always decreases sharply in December as people take their homes off of the market for the holidays. However, based on the data I’ve collected, this was the lowest level for inventory in at least three decades. The previous low was 1.43 million in December of 1993.

Bill McBride, Calculated Risk

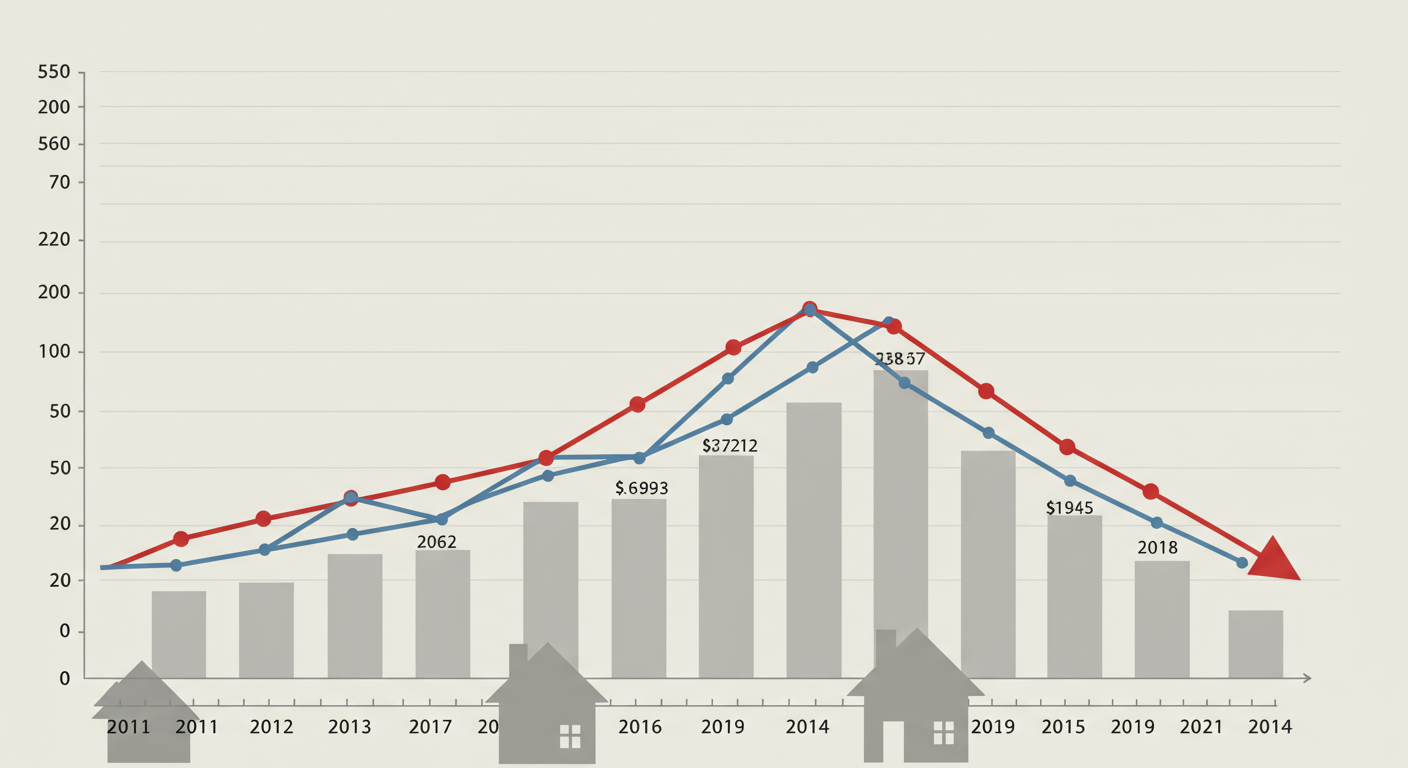

Above we show month’s supply of inventory going all the way back to 2011. Obviously, right after the housing crash, inventory skyrocketed. There were more and more houses coming on the market and less and less purchasers ready to purchase them. So, back between 2011 and 2012, we almost hit 10 months inventory. But then we’ve been steadily going down as the market has recovered. But if you take a look at where that red dot is right now, we can see we are at 3 months inventory, and that is hitting every price point.

New construction is picking up, which is fantastic, but it is still behind the curve. Above is the number of single-family construction homes over the last several decades (by a per million population). We have almost half of what’s been constructed in each of the previous 5 decades.

The sales pace on newly built single-family homes ended 2019 with a gain of 10%, increasing to a total of 681,000. This marks 2019 as the best year for new home sales since the Great Recession. New construction is a great way to become a first-time home seller. Most people who have already become first time homebuyers are now not selling, because of the inventory situation. New construction could be the answer to that.

A year ago, a combination of government shutdown, stock market slump, and mortgage rate spike caused a long-anticipated inventory rise. That supposed boom turned out to be a short-lived mirage as buyers came back into the market and more than erased the inventory gains. As a natural reaction, the recent slowdown in home values looks like it’s set to reverse back.

Skylar Olsen, Director of Economic Research at Zillow

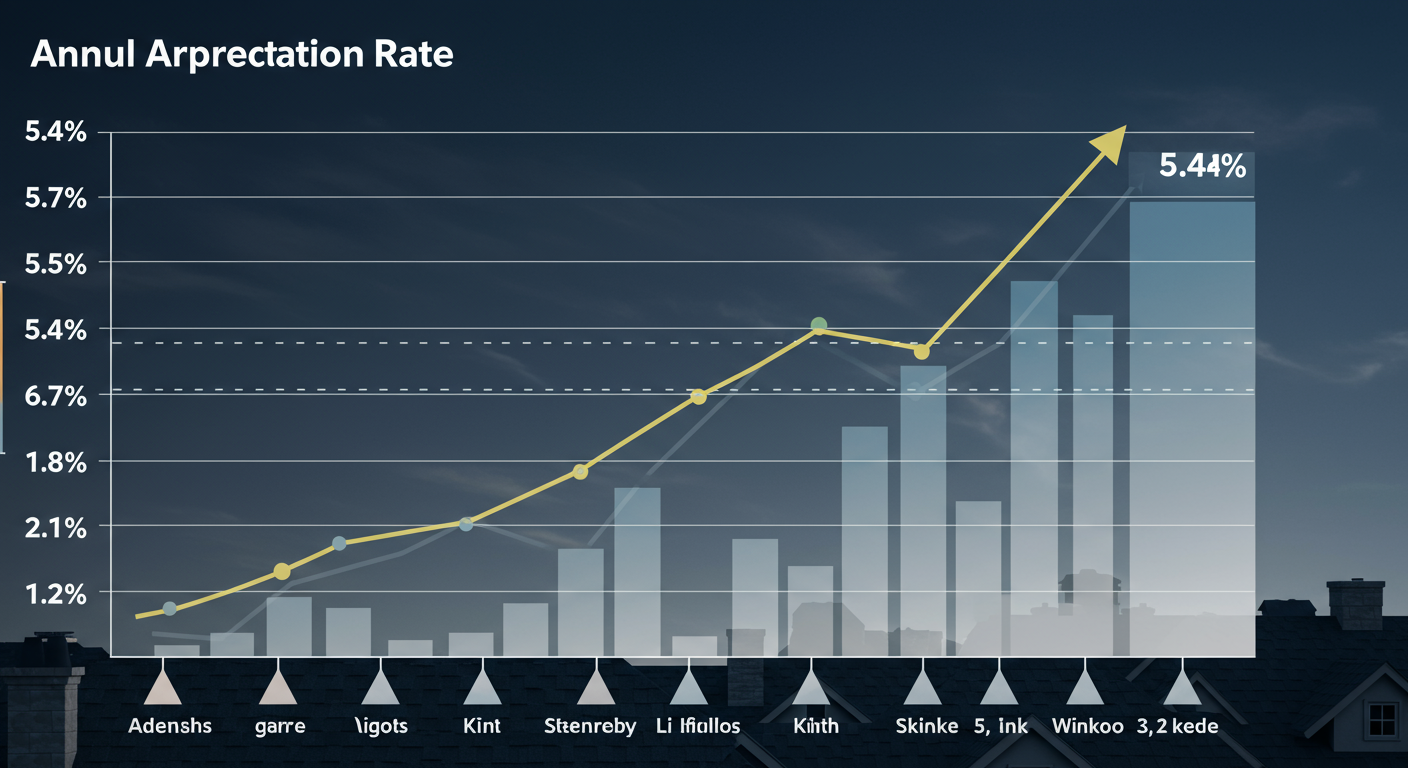

Historically, the annual appreciation in residential real estate is 3.6%. As you can see from the image above, prices are still very strong. CoreLogic is forecasting that across the United States, we are going to see 5.4% appreciation.

Above is a compilation of the experts projecting home price expectations over the next 3 years. We will most likely see prices continue to appreciate.

Well, if you’re planning on buying a house, home prices might look intimating. But, remember, just because you saw house prices that other people in the nation are buying, that doesn’t mean you should look for a house in that price range. Instead, focus on your own budget. Don’t worry about the pricing trends. A good real estate agent can help you find a home you love that’s within your budget.

Dave Ramsey, Financial Guru

Remember that even though prices are going up, that doesn’t mean the cost to you on a monthly basis is going up. Outside of home prices, there are other factors that can change your mortgage payment. Mortgage insurance requirements, the interest rate, down payment size, credit score, and debt-to-income ratio. The big one is interest rate. If interest rates are going down, even if prices are going up, you’re still going to be in good shape.

We expect mortgage rates to remain low over the next 2 years, averaging 3.8% in 2020 and 2021.

Freddie Mac

Above is the median seller tenure in their home since 1985 – how long have people have stayed in their houses. We can see from the beginning, all the way to 2008, people stayed in their house on an average of 6 years. But then after the crash, due to a lack of equity, people stayed in their houses much longer. Instead of averaging 6 years staying in their house, it jumped to 9 years. So, when building new construction wasn’t taking place over the last decade, the amount of existing homes that came to the market also decreased.

When it comes to home prices for sellers, the main question is: how much money can I make on my home sale?

Dave Ramsey, Financial Guru

The new numbers for 2019 just came out. Sellers realized a home-price gain of $65,500 on a typical sale. This marked the highest level in the U.S. in over 13 years. The average homeowner, when they sold their house, walked away with $65,000. This is a great time to sell your house.

Finally, I want to talk about the fact that when you hear “30-year mortgage,” and you’re 60 years old, you are probably thinking “Well, I don’t know if I could qualify now that I’m retired, and would a bank even give me a 30-year mortgage if I’m 60 years old?” Some retirees may wonder how they’ll qualify with limited monthly earnings. Lenders are now qualifying older adults for a mortgage based on their pensions, their social security dividends, and any interest that they’re getting. So, yes, there’s a very good chance that they’re going to be able to get a mortgage. Especially if they have a current house to sell.

So… what’s going on in Tallahassee?

1,093 NEW LISTINGS | $2220,964 AVERAGE SOLD LIST PRICE | $262,991 AVERAGE UNSOLD LIST PRICE |

|---|---|---|

480 SOLD | $214,187 AVERAGE SOLD PRICE | 98 AVERAGE DAYS ON MARKET |

PERCENTAGE LISTINGS SOLD | % SALES PRICE TO LISTING PRICE | PERCENTAGE HOMES EXPIRED |

Stay up to date on the latest real estate trends.

All Real Estate News

June 25, 2026

All Real Estate News

June 24, 2026

All Real Estate News

June 23, 2026

All Real Estate News

June 22, 2026

All Real Estate News

June 18, 2026

All Real Estate News

June 17, 2026

You’ve got questions and we can’t wait to answer them.