May 2024 Real Estate Market Update

May 19, 2024

Articles for Buyers

May 19, 2024

Articles for Buyers

This month we begin by focusing on one of the real estate market’s biggest concerns right now – affordability, which will lead us to get you information on where to find down payment assistance programs for first-time homebuyers and repeat buyers alike. Finally, we will discuss mortgage rates coming out of the latest Federal Reserve meeting, as well as an overview of how the employment data and inflation play into it all.

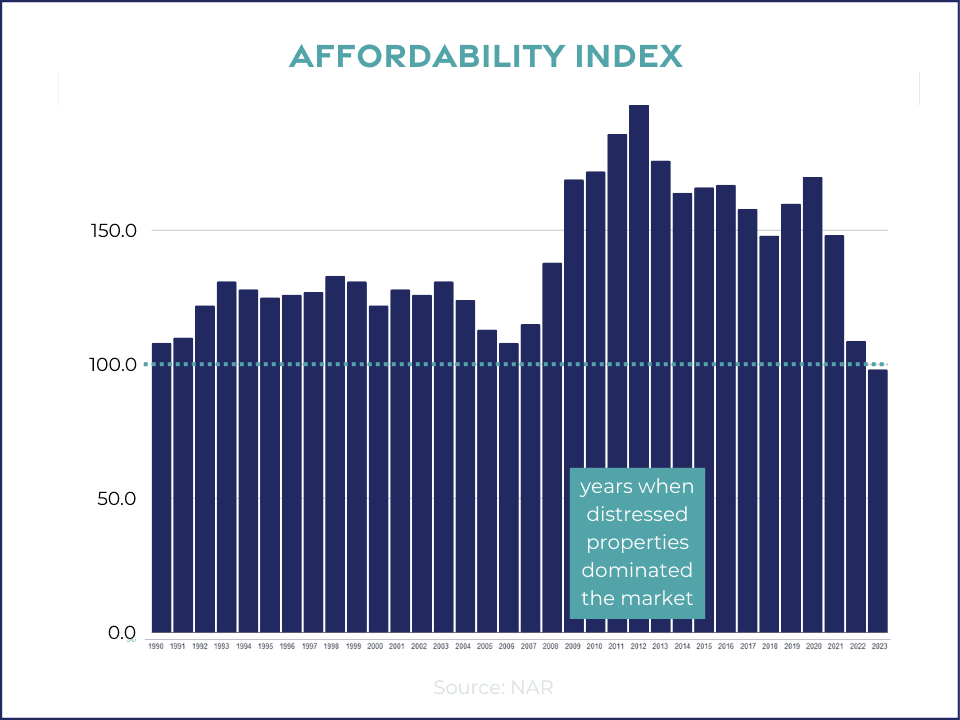

To dissect affordability, we turn to the National Association of REALTORS® Housing Affordability Index.

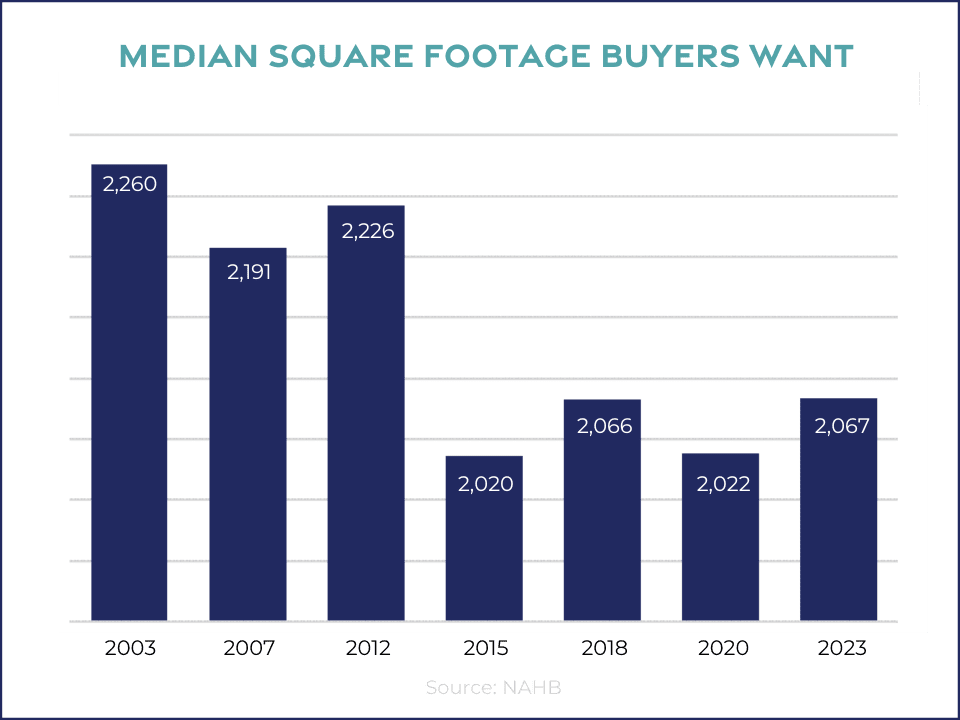

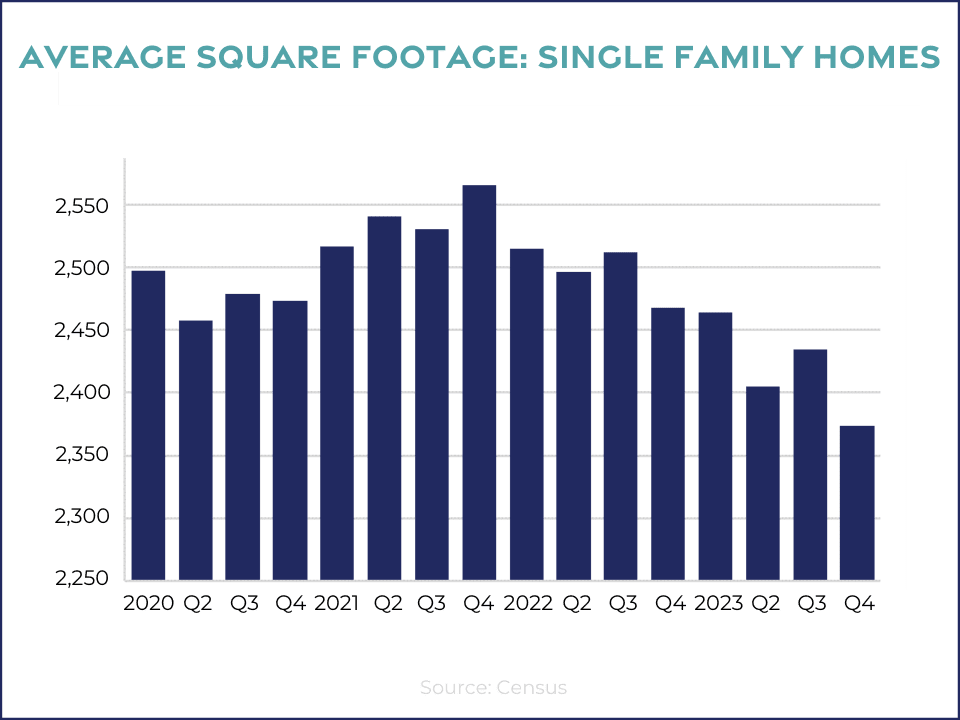

It is clear that homes are less affordable today than they have been, looking all the way back to 1990. A combination of rising prices, coupled with rising mortgage rates, makes affordability one of the market’s biggest concerns right now. However, builders are responding. One of the solutions they have recognized is building smaller homes. 38% of builders said they built smaller homes in 2023, and 26% have plans for smaller homes this year. There is a clear trend that buyers are interested in smaller homes.

After a brief increase during the post-COVID building boom, home size is trending lower and will likely continue to do so as housing affordability remains constrained.

National Association of Home Builders

Of the new inventory coming to market across the country, we are seeing more and more new construction than we have previously. In addition to building smaller homes, it is not uncommon to see builder incentives, and mortgage rate buy downs – both of which can be extremely beneficial for consumers.

Despite the affordability challenge, Chase was recently quoted saying,

According to a recent study from a major real estate brokerage, about 30% of 25-year-olds owned their own homes in 2022, 2-3% ahead of both millennials and Gen X at the same age.

By adopting the right strategies, like exploring down payment assistance programs, you can bring your dream of owning a home closer to reality. DownPaymentResource.com has an outstanding portal in which you can enter your information, and it will let you know how many and which down payment assistance programs may be available to you. There are over 2,000 affordable mortgage programs!

In Tallahassee, if you were looking to purchase a $250,000 home, there could be 23 down payment assistance programs available to you! Other things that may qualify you for particular programs are a military status, or a job in the education, law enforcement, firefighter, or healthcare fields.

Overall, 39% of the programs are for repeat buyers, and 75% provide down payment and closing cost assistance.

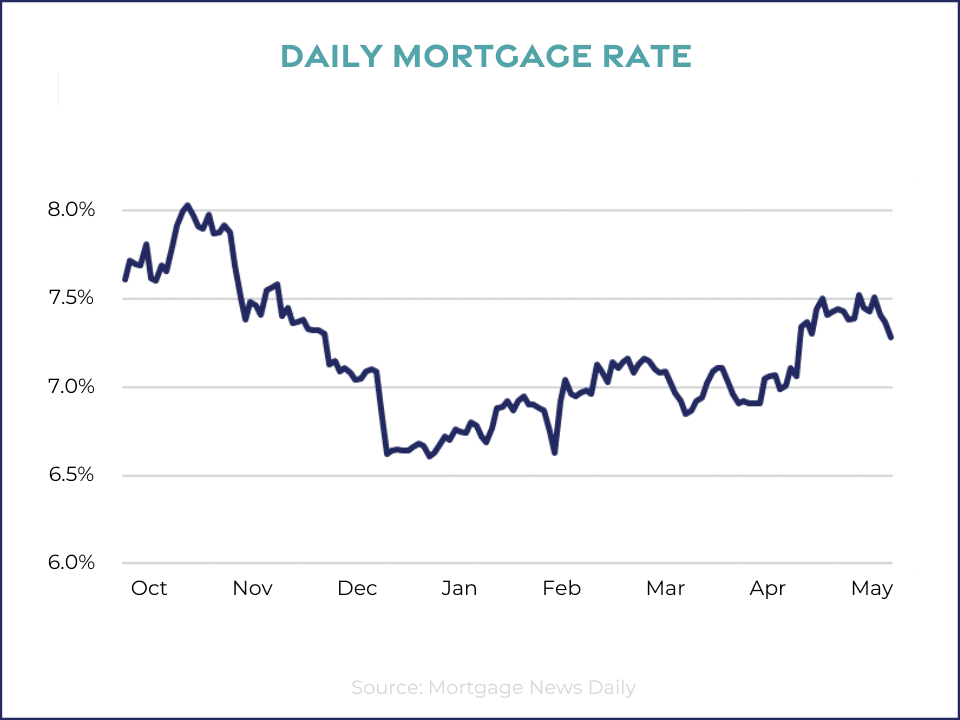

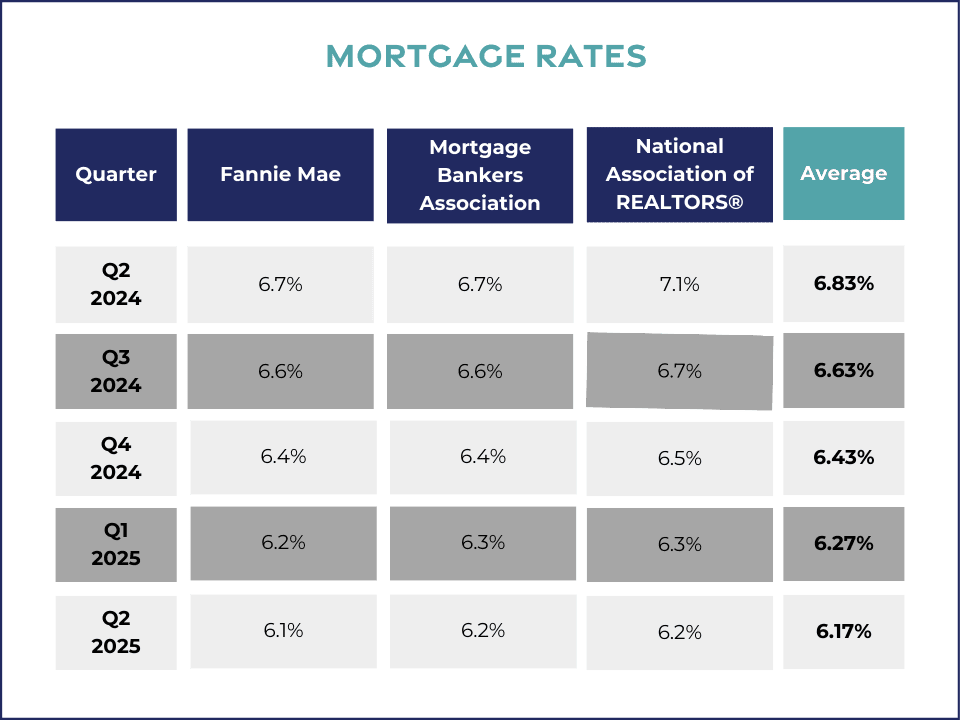

The biggest thing when we're looking at mortgage rates right now is volatility.

Nicole Bachaud, Senior Economist, Zillow

The bottom line is that it is going to take a little bit longer for mortgage rates to come down. To understand why, let’s look at the mortgage rates since October 2023 – when the rate peaked at 8%.

For 4 months, we were in a downward trending environment, and have spent 3 months seeing an upward trend. The Federal Reserve does not simply set mortgage rates. There are many factors that play into it.

Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.

Odeta Kushi, Deputy Chief Economist, First American

To understand it better, you have to look at the leading indicators of mortgage rates:

Mortgage rates are influenced by many elements, including the inflation rate, the pace of job creation, and whether the economy is growing or shrinking. The Federal Reserve's monetary policy is a factor, too, and is set by the Federal Open Market Committee.

Nerd Wallet

Mortgage rates are indirectly influenced by the Federal Reserve’s monetary policy. When the central bank raises the federal funds target rate, as it did throughout 2022 and 2023, that has a knock-on effect by causing short-term interest rates to go up.

Forbes

So, the Federal Reserve doesn’t actually set mortgage rates, but their actions indicate what's happening in the broader economy – to which mortgage rates respond.

The Federal Reserve has been raising the federal funds rate in an effort to slow the economy. Raising the federal funds rate essentially makes it more expensive to borrow money. There was an anticipation that the Federal Reserve may be starting to cut the federal funds rate in the first half of this year, however they may need to see more definitive trends (and a slowing of the economy) for that to happen.

The Federal Reserve said the committee's assessment will take into account a wide range of information, including labor market conditions, inflation pressures, inflation expectations, and financial/international developments. These are the factors that impact mortgage rates.

The Fed is looking for signals the economy is cooling. Things like a strong job market, but maybe not as strong as predicted.

Nonfarm payrolls increased by 175,000 on the month, below the 240,000 estimate from the Dow Jones consensus . . . The unemployment rate ticked higher to 3.9% against expectations it would hold steady at 3.8%.

CNBC

In April, the actual number of new jobs and the unemployment rate are both strong figures, but fell below the expectation – signs of the economy cooling.

When it comes to the unemployment data, we saw job growth in the education, healthcare, retail, construction, manufacturing, and transportation industries.

Today’s cooler labor market data is a sign that mortgage rate relief could be on the horizon, but that will be dependent on inflation… we may see an unseasonably active summer and fall if inflation improves and mortgage rates drop…

Danielle Hale, Chief Economist, Realtor.com

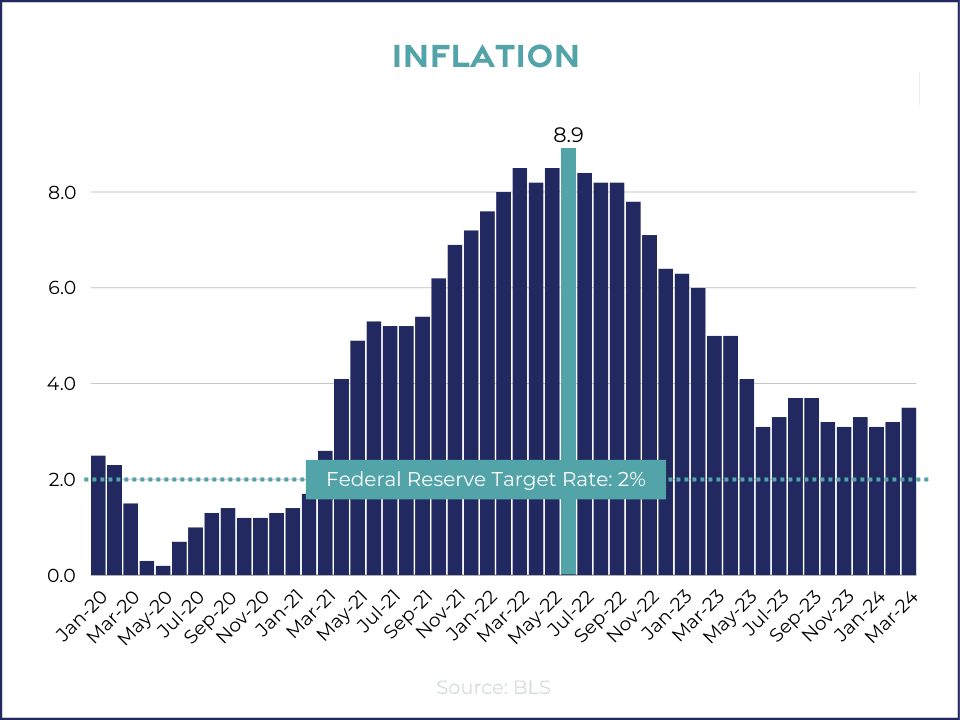

Inflation today continues to exceed the Federal Reserve's target rate.

While we are not at the Federal Reserve’s target rate of 2%, we are also far from the 8.9% in June of 2022. Raising the federal funds rate has helped to slow the economy. Inflation is coming down. Recently, inflation came in higher than expected. Again, high inflation tends to mean high mortgage rates.

We expect mortgage rates to drop later this year, but not as far or as fast as we previously had predicted.

Mike Fratantoni, Chief Economist, Mortgage Bankers Association

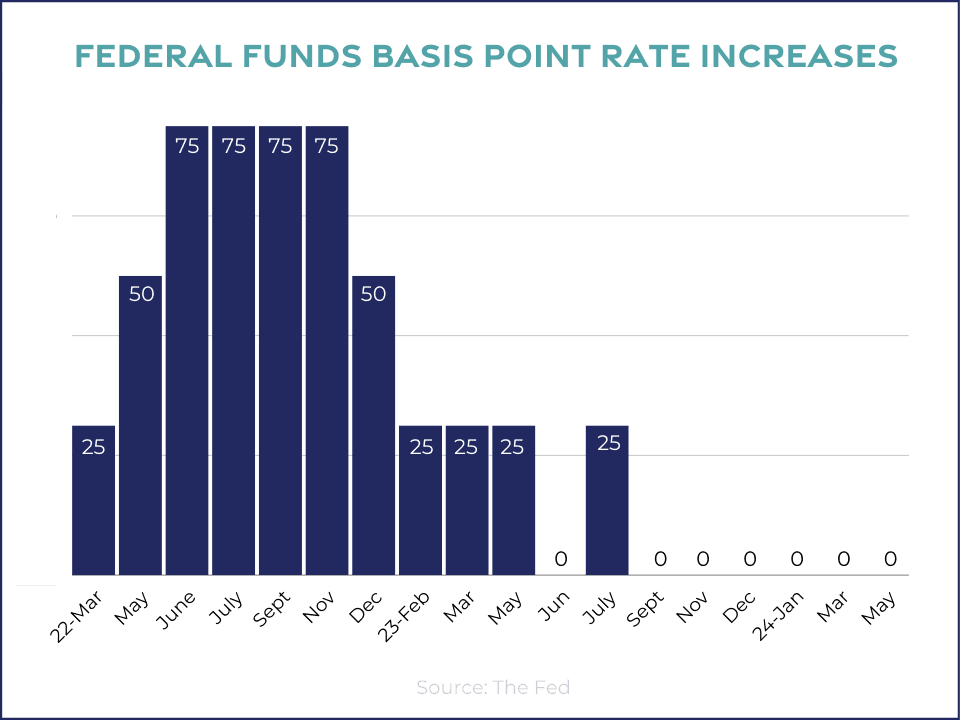

Looking at the federal funds rate increases over the past two years, they are much less aggressive than they have been.

Essentially, the Federal Reserve cannot move too quickly, and need to watch the data.

Reducing policy restraint too soon or too much could result in a reversal of progress we have seen in inflation and ultimately require even tighter policy to get inflation back to two percent.

Jerome Powell, Chairman, Federal Reserve

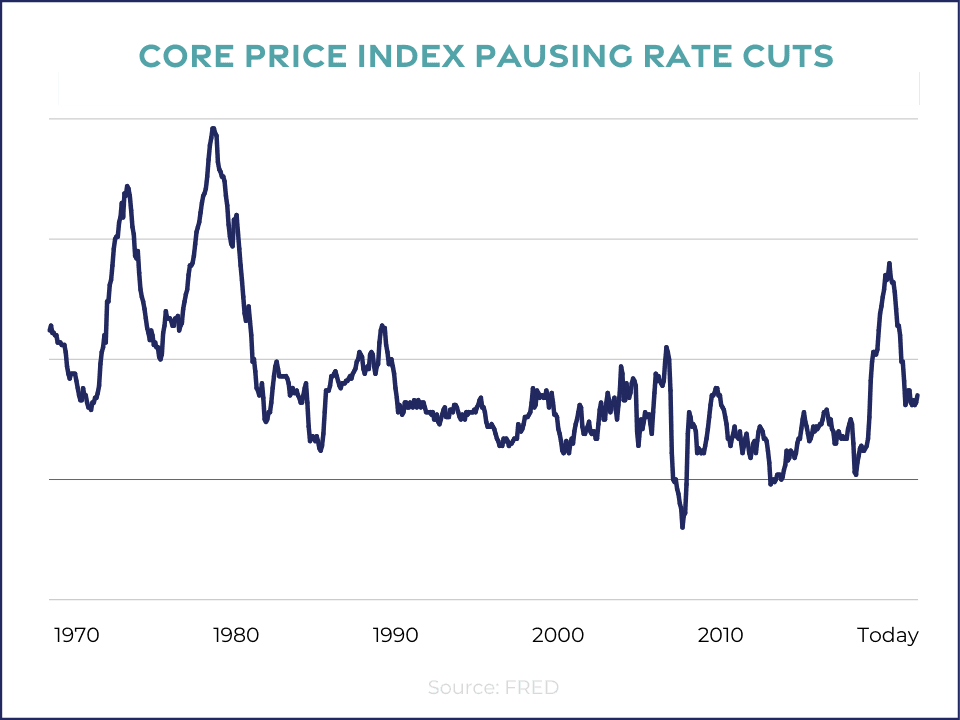

The Core Price Index is one of the measures of inflation that the Federal Reserve looks at. In the 1970s inflation was rising, so the Federal Reserve had to raise the federal funds rate to bring inflation down. However, they did it just a little too early – causing that second peak in the graph below.

When they cut too early, inflation spikes back up and they have to start all over again. We do not want to be in that position today. Fast forward to today: inflation was rising, the federal funds rate was increased, inflation started to come down, the last couple of readings came in just a touch higher than expected. The Fed does not want to repeat history. They are buying a little bit more time to make sure they're really seeing those consistent trends of a slowing in the economy.

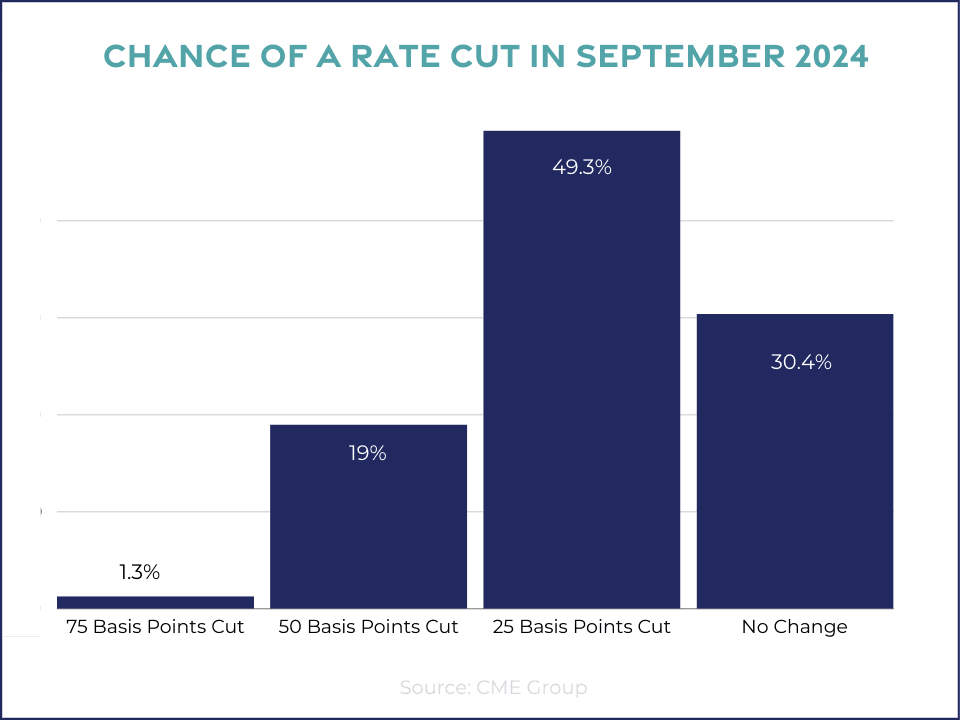

According to the CME Group, there's a 69.6% chance that the Federal Reserve cuts the federal funds rate at the September meeting.

I think it’s unlikely that the next policy rate move will be a hike.

Jerome Powell, Chairman, Federal Reserve

Overall, mortgage rates should continue to trend downward this year, and into next year.

Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.

Bright MLS

Stay up to date on the latest real estate trends.

All Real Estate News

June 25, 2026

All Real Estate News

June 24, 2026

All Real Estate News

June 23, 2026

All Real Estate News

June 22, 2026

All Real Estate News

June 18, 2026

All Real Estate News

June 17, 2026

You’ve got questions and we can’t wait to answer them.