November 2022 Real Estate Market Update

November 20, 2022

Monthly Market Updates

November 20, 2022

Monthly Market Updates

The hot topics in the housing market right now are mortgage rates and home prices, but we also want to touch on foreclosures and what that looks like nationally. Then, we’ll wrap up by shedding some light on if now is a good time to buy a home.

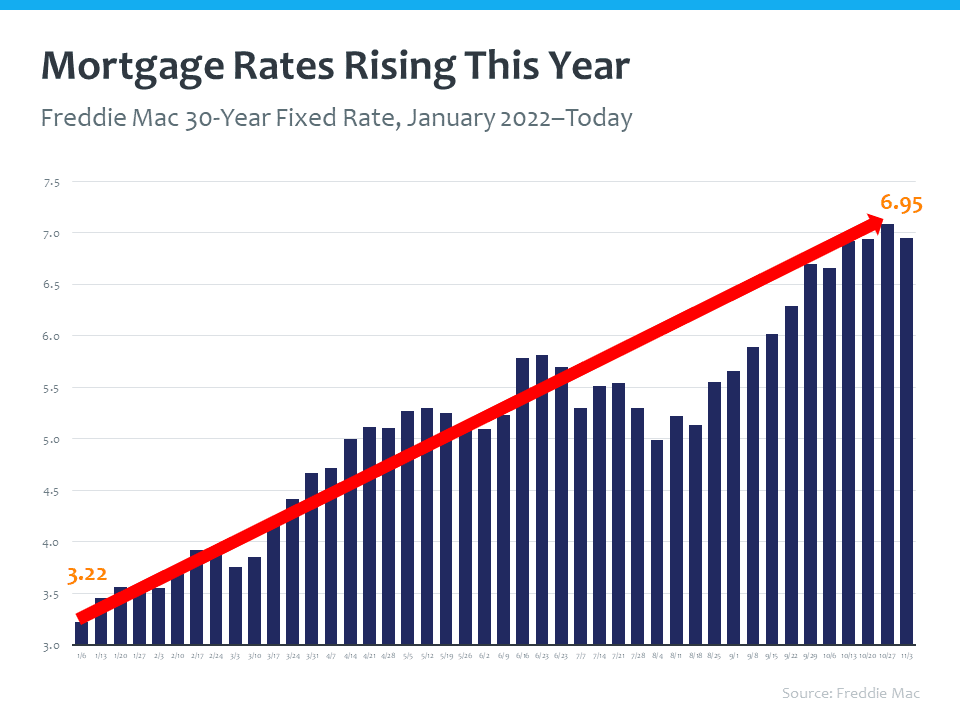

The biggest concern with mortgage rates right now is if they will continue to rise. This is a graphical representation of the Freddie Mac 30-year fixed rate from the beginning of the year to the second week of November. We can see that drastic incline in mortgage rates this year, which is causing the cool down in the market.

This is all about inflation. The Federal Reserve is making moves to raise the federal funds rate in an effort to lower inflation. They’re trying to slow down the economy. And in doing so, while the Fed does not call mortgage rates, mortgage rates tend to respond. While inflation is high, mortgage rates are going to remain high, so it is likely there will be an upward pressure on mortgage rates as we wrap up this year.

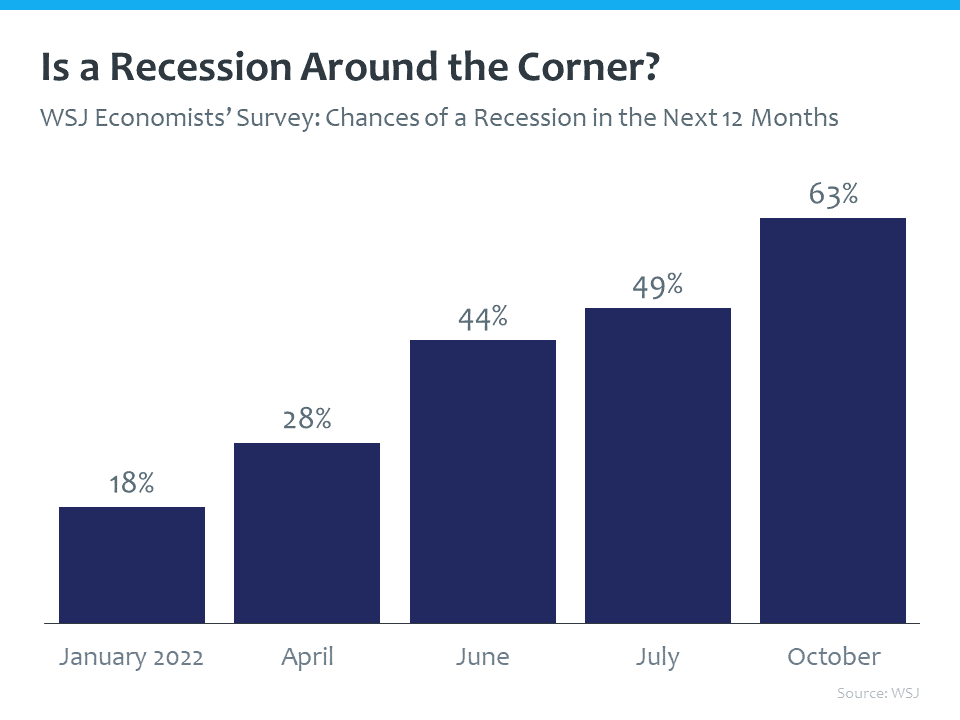

The Wall Street Journal asked economists, “What are the chances of a recession happening in the next 12 months?” The percentage of economists who are expecting a recession over the next 12 months has continued to increase since the beginning of the year. As of last month, 63% of economists feel that there’s going to be a recession sometime over the next 12 months. But remember that a recession does not mean falling prices.

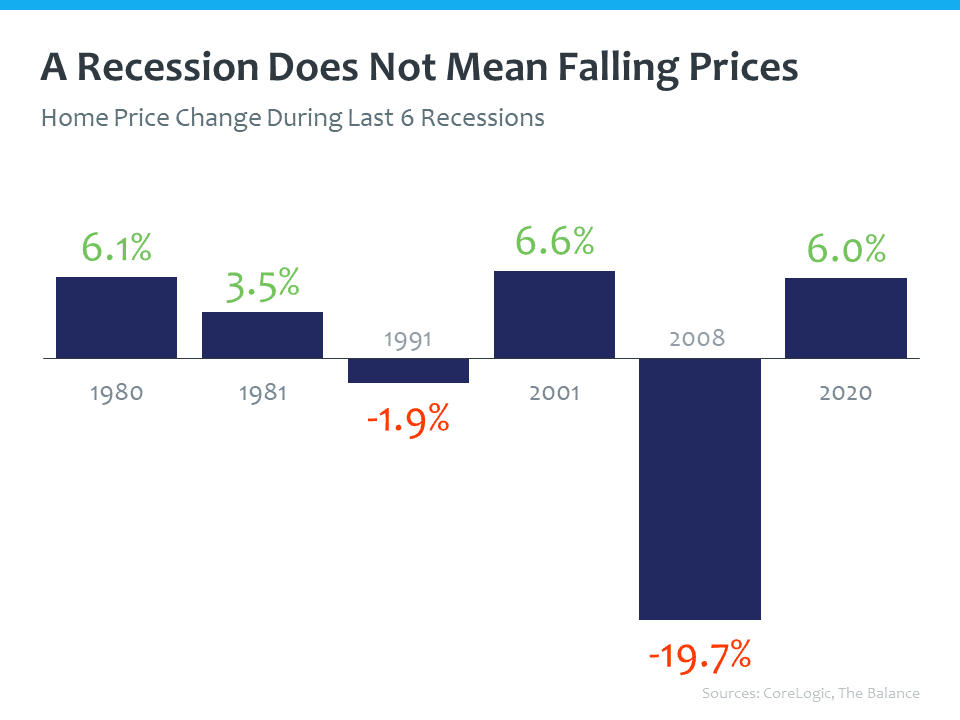

In four out of the last six recessions, home prices actually increased. Of course 2008 was an outlier, and a very different landscape from where we are now when it comes to inventory, lending standards, and equity – factors that are driving the housing market in a different direction. We don’t want to assume that we will not see falling prices, but this does show a recession does not mean home prices will fall.

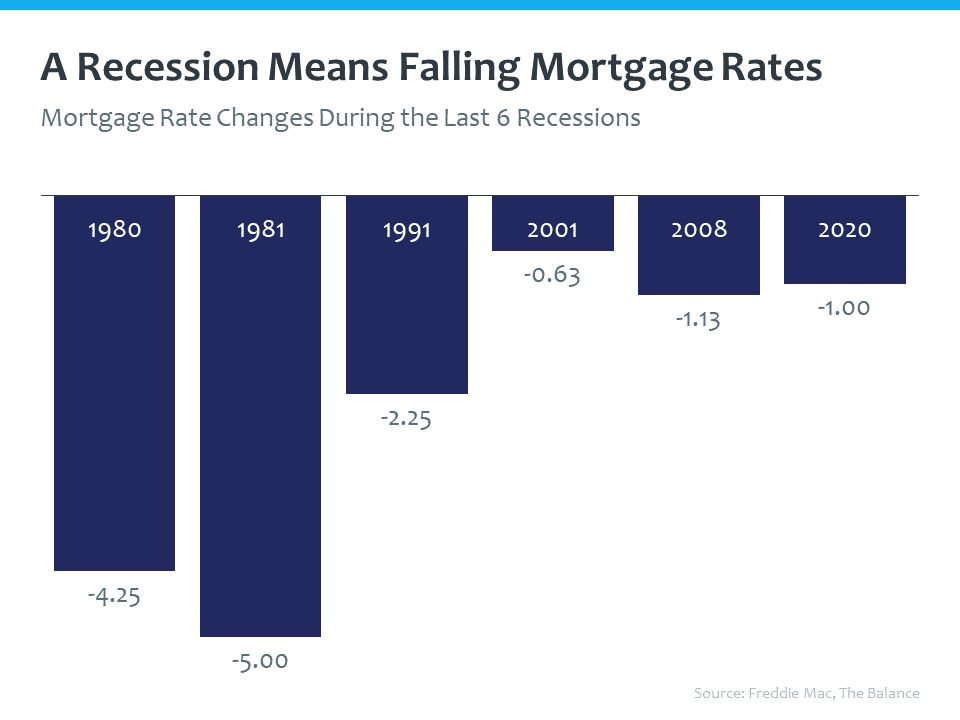

A recession also tends to coincide with falling mortgage rates. Of those same six recessions, mortgage rates dropped.

It is still a seller’s market, which is continuing to put an upward pressure on home prices. However, as the market shifts, more opportunities are opening up for buyers.

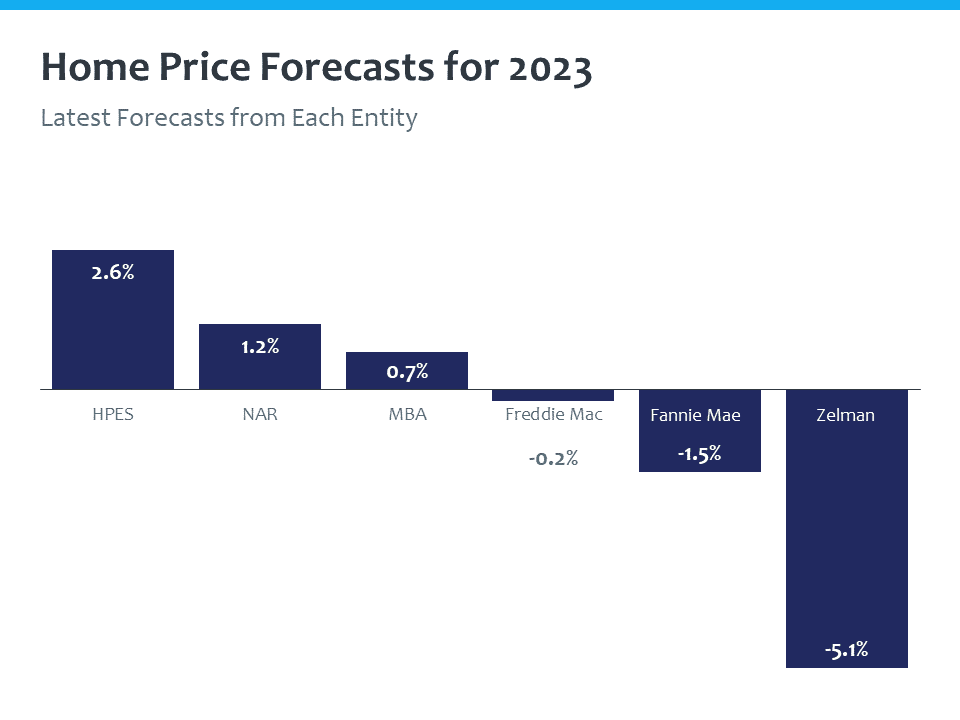

These are the Home Price Forecasts from the top 6 industry experts – the Home Price Expectations Survey (HPES), the National Association of Realtors® (NAR), the Mortgage Bankers Association (MBA), Freddie Mac, Fannie Mae, and Zelman. Overall, the predictions are a little bit up and a little bit down – on average a roughly neutral, flat home price appreciation for 2023.

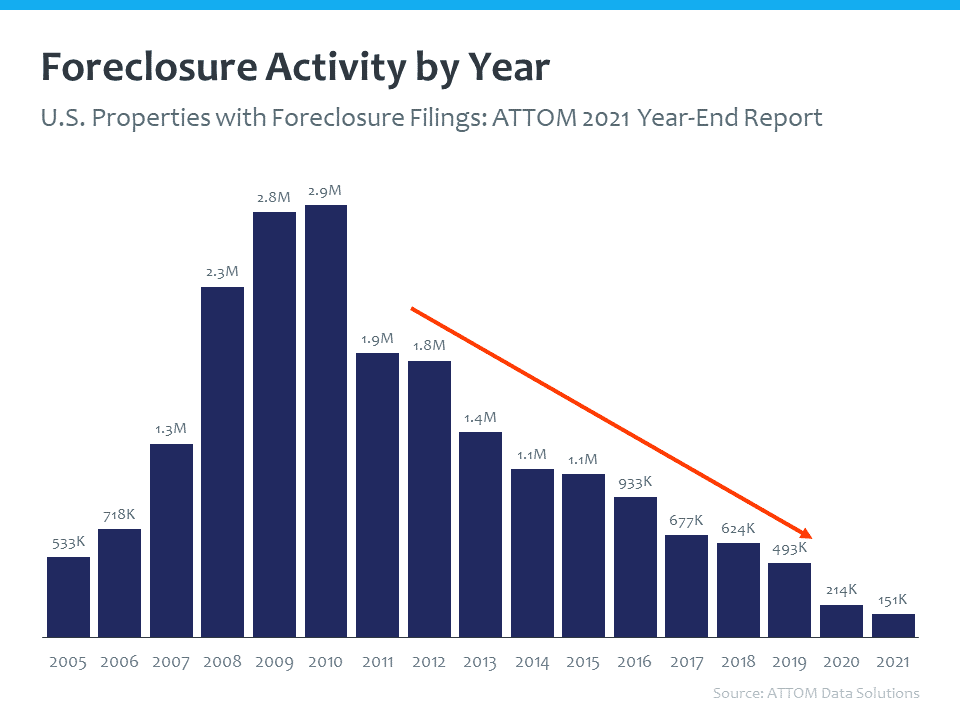

Moving on to foreclosures… this is the foreclosure activity by year from ATTOM Data since 2005. Foreclosures have drastically declined since 2010, because of the strict lending standards that were put into place after the financial crisis in 2008. Better qualified borrowers and stricter standards mean less defaults. One of the leading indicators of foreclosures is delinquencies, which are also down right now.

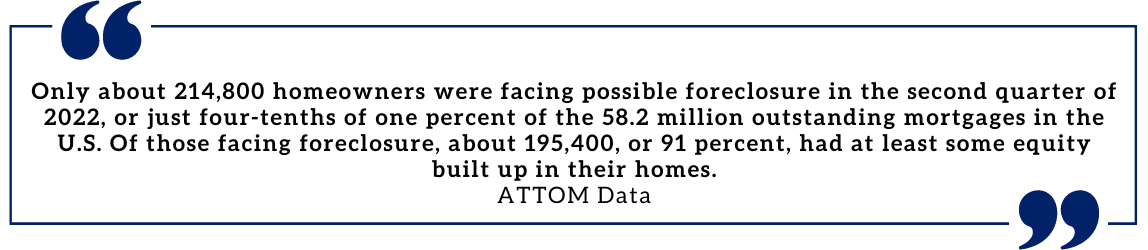

If you were to sit down with a servicer in the mortgage business, they would generally tell you they’re okay with about 1% default rate in a portfolio. Right now we are at four-tenths of a percent. In addition, of those facing foreclosure, 91% had equity. This equity could allow a homeowner to sell rather than foreclose.

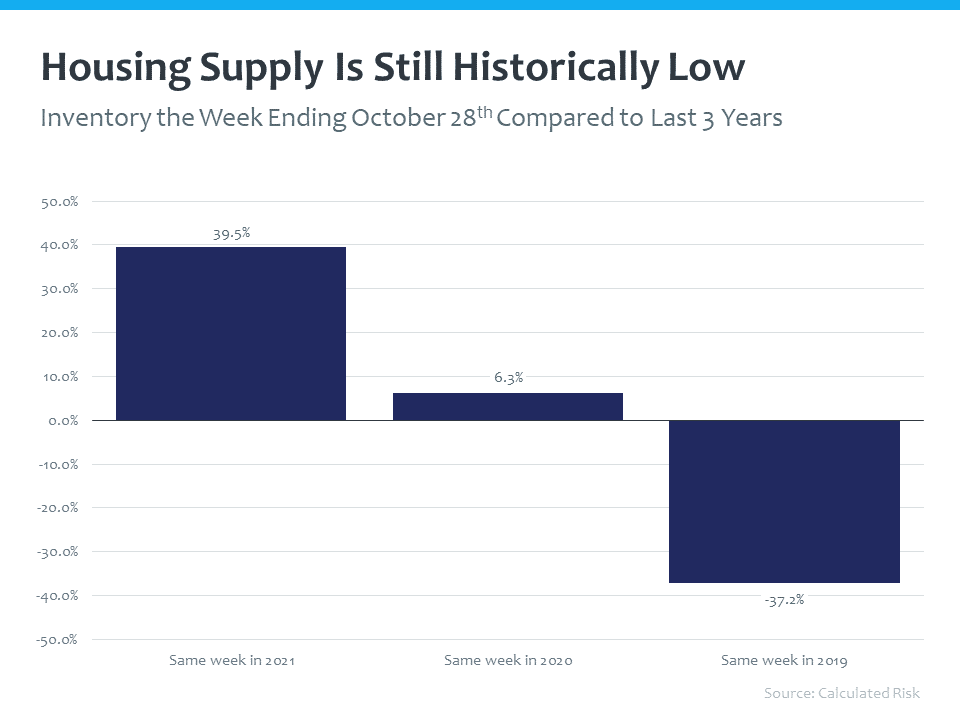

So, are we about to see a wave of inventory hit the market? Looking at the latest data from October, housing supply is up almost 40% from 2021, and about 6% from 2020. However, we are down almost 40% from 2019 – one of the “normal” years in real estate. Overall, we are still undersupplied across the country.

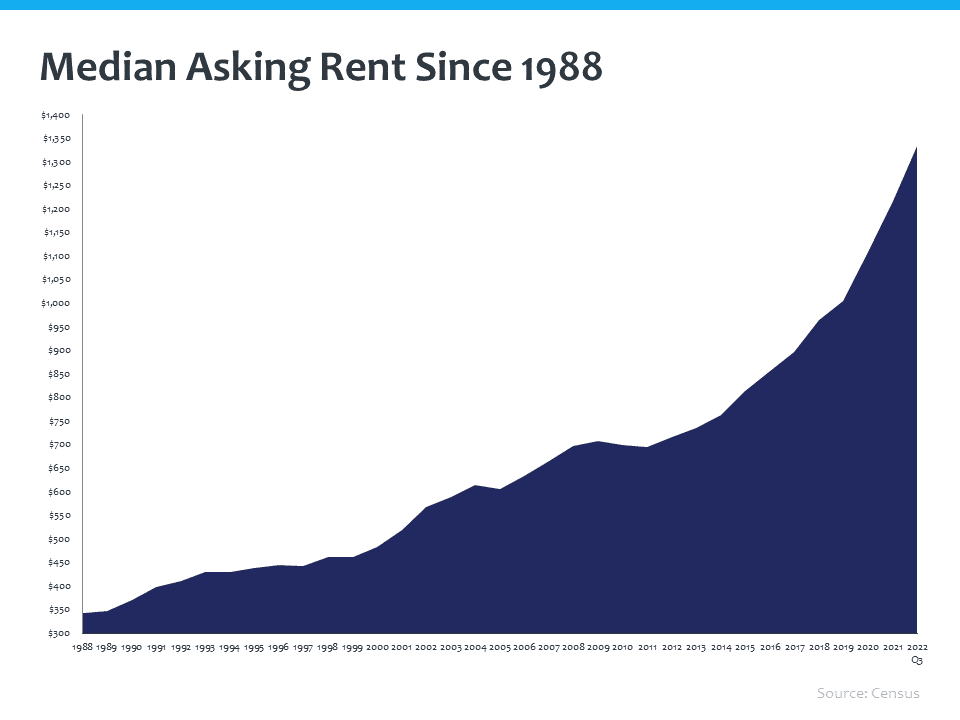

All this said, is it a good time to buy a home? This is a question only you can answer. It’s important to be educated on the market and where is it projected to go in order to decide if a home purchase is the right choice for you. But, if renting is the alternative, keep in mind that the median asking rate for rent has skyrocketed. Rental inventory is impacted by supply and demand, just like housing is. If you’re in the rental, then you can’t afford to save for a down payment to purchase a home, which then allows you to build wealth over time.

Stay up to date on the latest real estate trends.

All Real Estate News

July 9, 2026

Articles for Buyers

July 8, 2026

All Real Estate News

July 7, 2026

All Real Estate News

July 6, 2026

All Real Estate News

July 2, 2026

All Real Estate News

July 1, 2026

You’ve got questions and we can’t wait to answer them.