The top three concerns in the housing market right now are mortgage rates, home prices, and affordability.

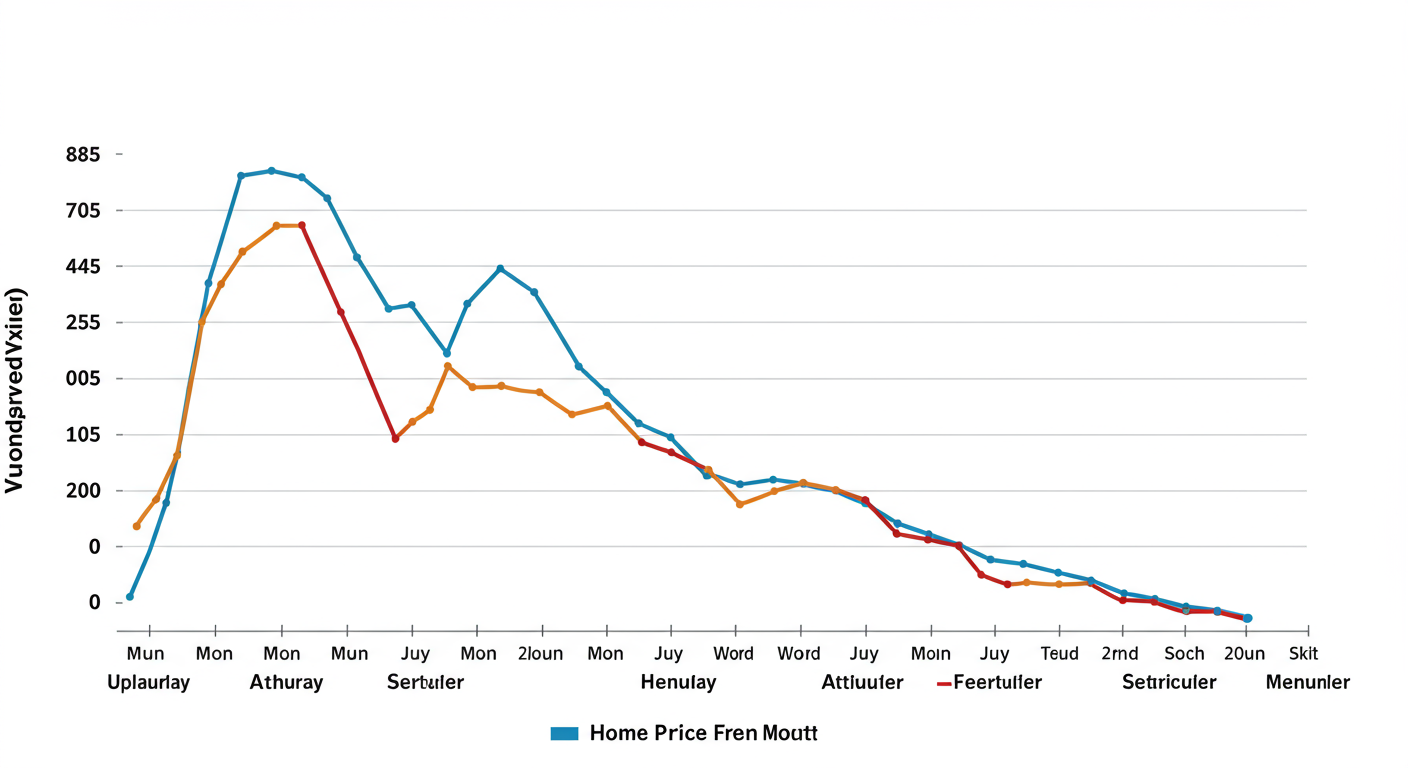

This year the housing market has truly been defined by rising mortgage rates. Taking a look at the Freddie Mac 30-year fixed rate, we can clearly see the jump earlier this year from 3.22% to over 5%. There has been a tremendous amount of volatility in mortgage rates over the past few months. This is because inflation is the enemy of long-term interest rates. The Federal Reserve is making moves to ease inflation, and when that happens mortgage rates respond.

The general consensus is that the Federal Reserve is going to get inflation under control. If that’s the case, then mortgage rates will stabilize to about 5.3%, and then dipping below 5% in the third quarter of next year.

Home prices are appreciating, but at a slower, more moderate rate than we have seen recently.

Nationally, home prices will continue to rise due to buyer demand and low inventory.

Home prices are slowing – not depreciating, and that’s where deceleration comes into play. We saw record-breaking home-price appreciation at the beginning of this year, and we have recently seen (and will continue to see) a deceleration of home prices. The pace of appreciation is slowing. That’s deceleration. It’s not depreciation – where we would have negative price growth. We will see continued appreciation at a slower pace. This gives buyers a little bit more negotiating power.

The past two years have been an anomaly. The price growth over the past year was unsustainable.

Many experts raised their home price forecast this year. Most likely because of the continued low inventory levels and the increasing mortgage rates.

We are looking at 11.3% annual home price appreciation for 2022, keeping in mind a lot of that already happened at the beginning of this year.

Inventory is 26.3% higher than it was last year, which creates more opportunities for buyers. However, compared to the same week in 2020, inventory is down 5.4%, and down 42.2% from the same week in 2019. Historically, inventory is still low, and that’s what’s continuing to drive an upward pressure on home prices.

Housing affordability is lower than it’s been since the early 1990s. The National Association of Realtors® Housing Affordability Index, is based on 3 things: home prices, interest rates, and wages – where the higher the bar, the more affordable a home. A reading of 100 is an even reading – where the average household can afford 100% of the average mortgage payment. As right now, the average household can afford 98.5% of the average mortgage payment – so, unaffordable.

Compared to one year ago, the monthly mortgage payment rose from $1,265 to $1,944 – an increase of 53.7%. There is no doubt that homes are less affordable right now.

Another thing that we want to look at when we start to break down affordability is the average mortgage payment, or income committed to a mortgage payment, which sits at 25.4%. This assumes a 30-year fixed mortgage rate with a 20% down payment on a median-priced home with median income. 25.4% of income is dedicated to a housing payment, where 25% is typically what is recommended.

Taking a look at median household income versus qualifying income – what you need to make to buy a home, is pretty even for the South which is following the national trend.

To combat the current housing affordability right now, buyers can expand their search area and criteria – maybe consider looking a little bit further out of their desired area. Or explore alternative financing options with several different lenders. Finally, buyers can look for grants at sources like

DownPaymentResource.com.